|

educational blogs |

|

THIS IS NOT A TIP OR RECOMMENDATION. I AM NOT A TIPSTER. PLEASE DO YOUR OWN RESEARCH. PLEASE READ THE DISCLAIMER ON THE HOME PAGE OF MY WEBSITE. IF YOU COPY MY TRADES, YOU WILL PROBABLY LOSE MONEY. I HAVE A LARGE PORTFOLIO AND I USE DIVERSIFICATION TO SPREAD RISK ALONG WITH TRICKS LIKE HEDGING AND OCCASIONALLY BY THE USE OF STOPLOSSES - IF YOU BUY ANY STOCK YOU REALLY SHOULD FOCUS ON HOW IT FITS IN WITH THE REST OF YOUR PORTFOLIO AND KEEP RISK MANAGEMENT AT THE FOREFRONT OF EVERYTHING YOU DO. BE AWARE THAT ALL INVESTORS/TRADERS GET THINGS WRONG AND MANY STOCK SELECTIONS WILL WORK OUT BADLY.

You have probably noticed that this is Part 2 of the Blogs – if you have not read Part 1 yet you can find it here: http://wheeliedealer.weebly.com/educational-blogs/stock-idea-hotel-chocolat-hotc-part-1

Recent Trading

You can read HOTC Interim Results here which came out on 26th February 2019: https://www.hotelchocolat.com/on/demandware.static/-/Sites-HotelChocolat-Library/default/dw953a5b02/FY1819InterimRNSFinal.pdf There is also a Presentation of these Interim Results here: https://www.hotelchocolat.com/on/demandware.static/-/Sites-HotelChocolat-Library/default/dwd7bbeece/HCFY19interimFinal.pdf From looking through these Results, the following bits stand out to me:

SharePad ‘Phil Oakley’ Charts SharePad has some really useful Charts that Phil Oakley set up before he defected to Investors Chronicle. The Screen below shows where you can find these Charts (bottom right) but I will blow the Charts up in size for any I include in this Section and also note that I took this image on the 22nd June 2019 and some of the numbers might look out of date – but for our purposes it shouldn’t matter much.

Here’s the first one – clearly HOTC is showing nice Revenue and Profit growth.

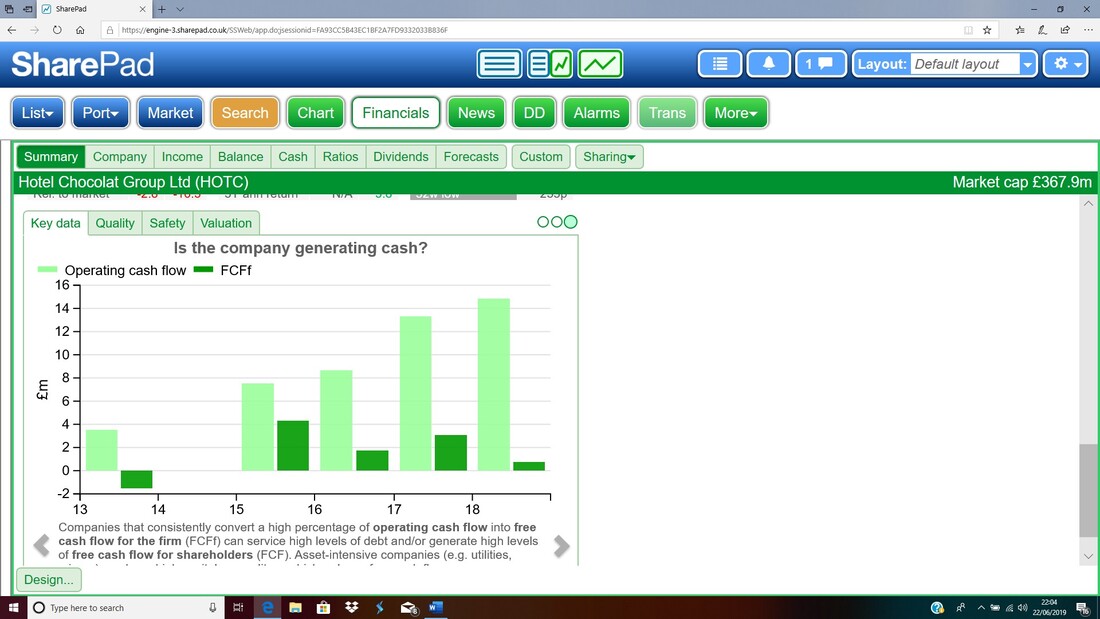

Obviously we are a bit limited because HOTC has not been listed on the Stockmarket for all that long but next I will show a Cashflow Chart. Of course other more established Stocks on SharePad have a lot more information in their Charts.

This next Chart which I have selected is interesting. On the face of it things do not look all that impressive but read the note at the bottom and I suspect it is the case that Free Cashflow is being hampered by Capital Investment in new Stores etc.

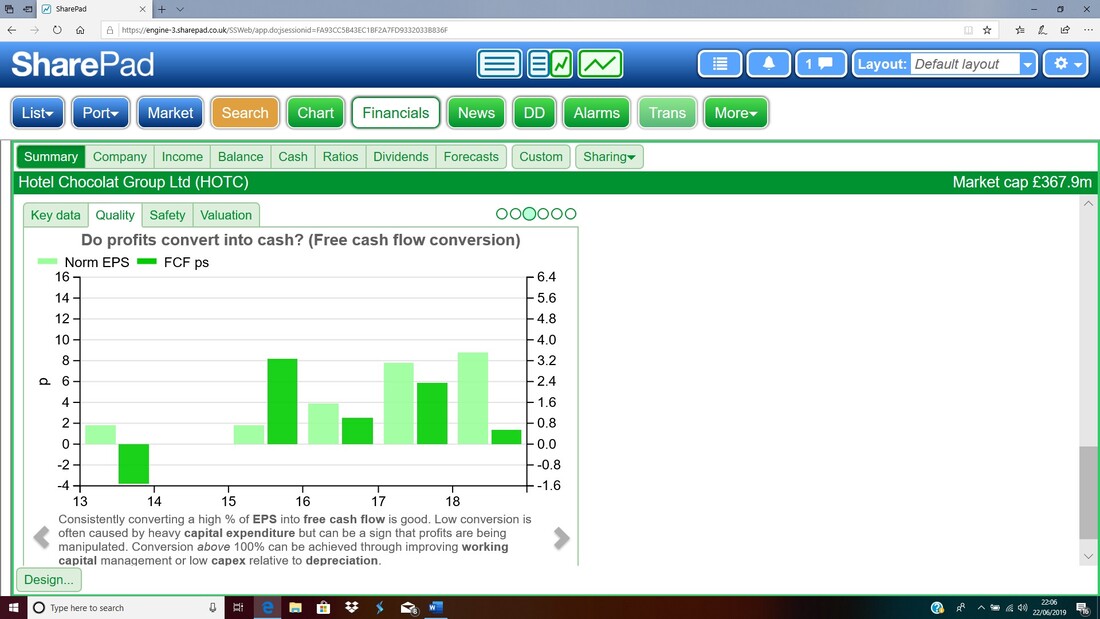

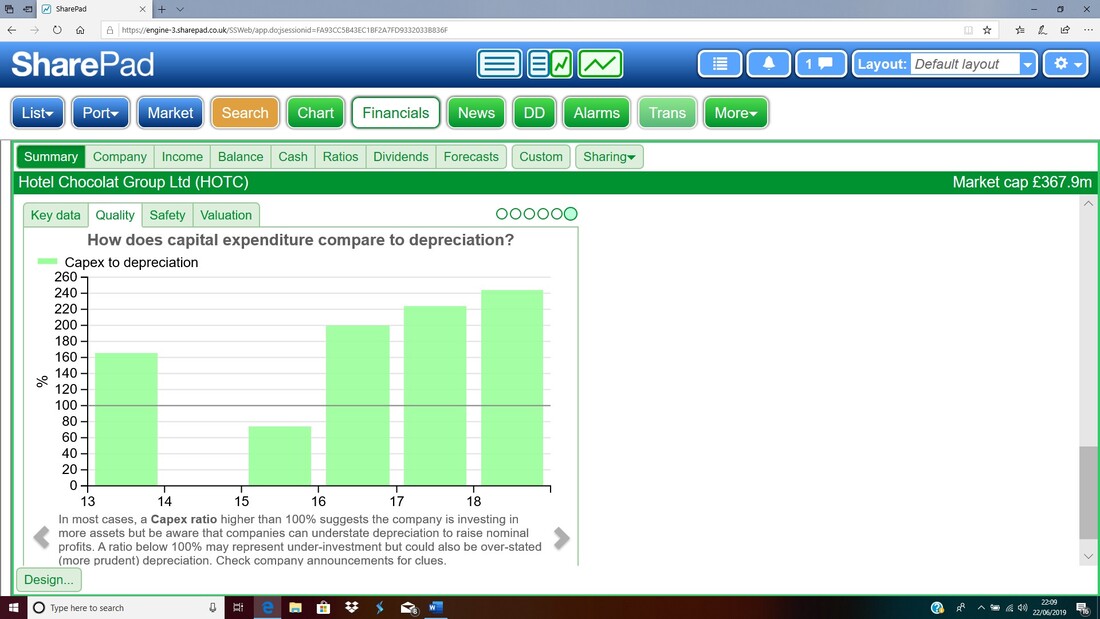

On the next Chart it is again worth reading the text at the bottom. In this case it looks like the Capex is high due to new Stores again.

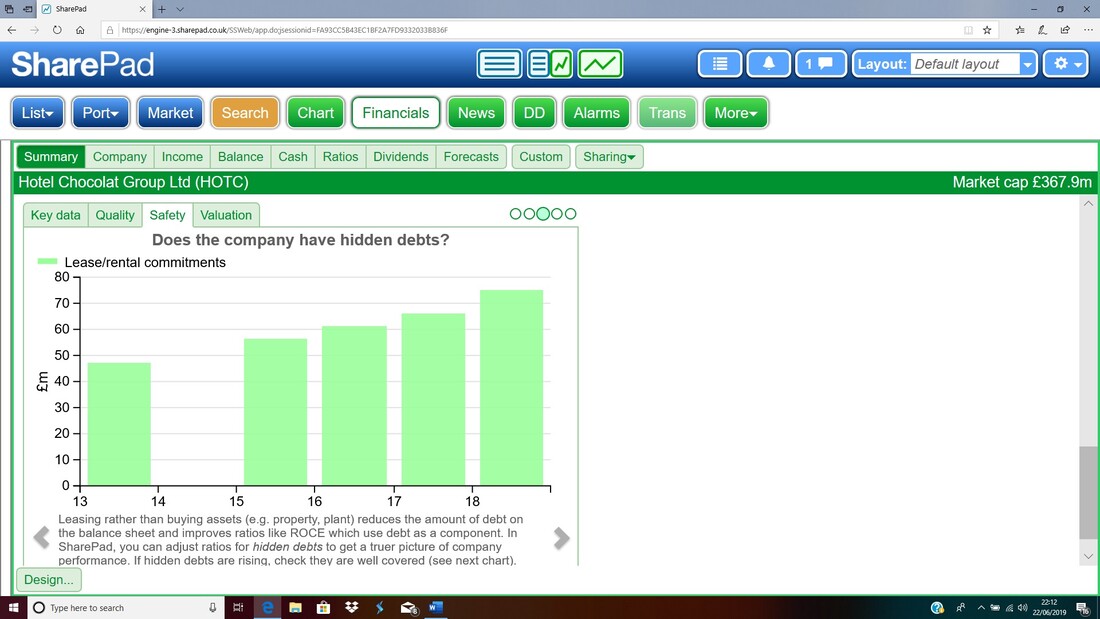

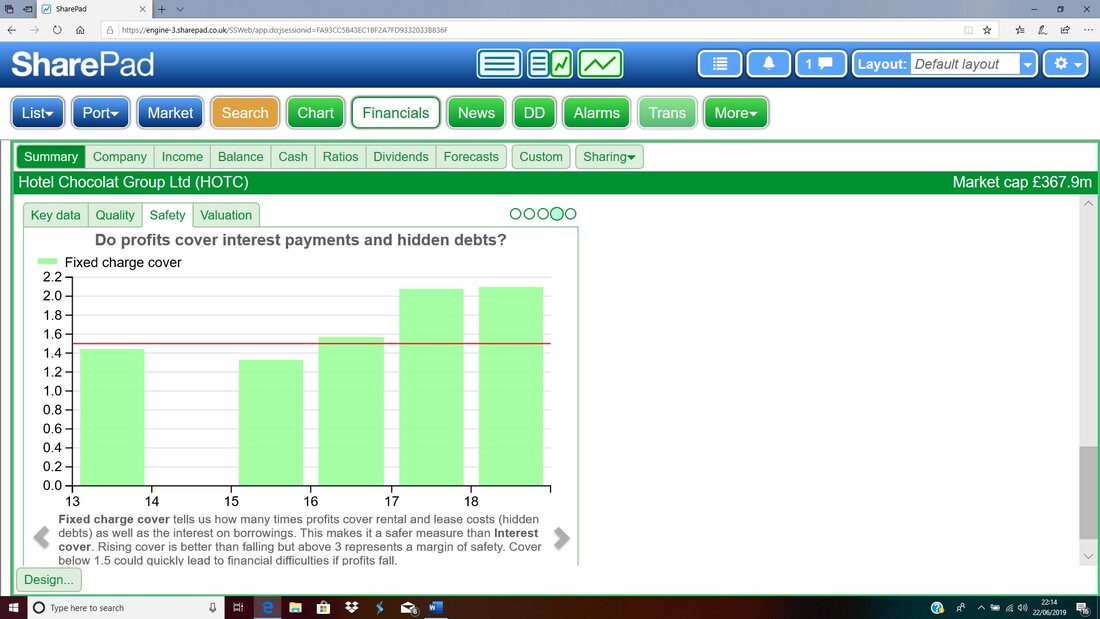

This next Chart is quite topical because it is to do with Lease Commitments and recently the Accounting Standards were changed so that Companies had to bring Leases onto their Balance Sheets. Clearly the Lease Commitments are rising as more Stores are opened.

Again it is worth reading the text at the bottom of this next Chart. The Red Horizontal Line represents the 1.5 times level and the text at the bottom explains anything below this as potentially dangerous if Trading goes smelly. In the case of HOTC we seem to have rising Cover which is good but it is not up to the 3 times level that Phil Oakley says provides a ‘Margin of Safety’.

I have not included any of the ‘Valuation’ Charts as they all look ugly !! I have mentioned before that HOTC cannot be described as ‘cheap’ but I will discuss the Valuation situation in the next section.

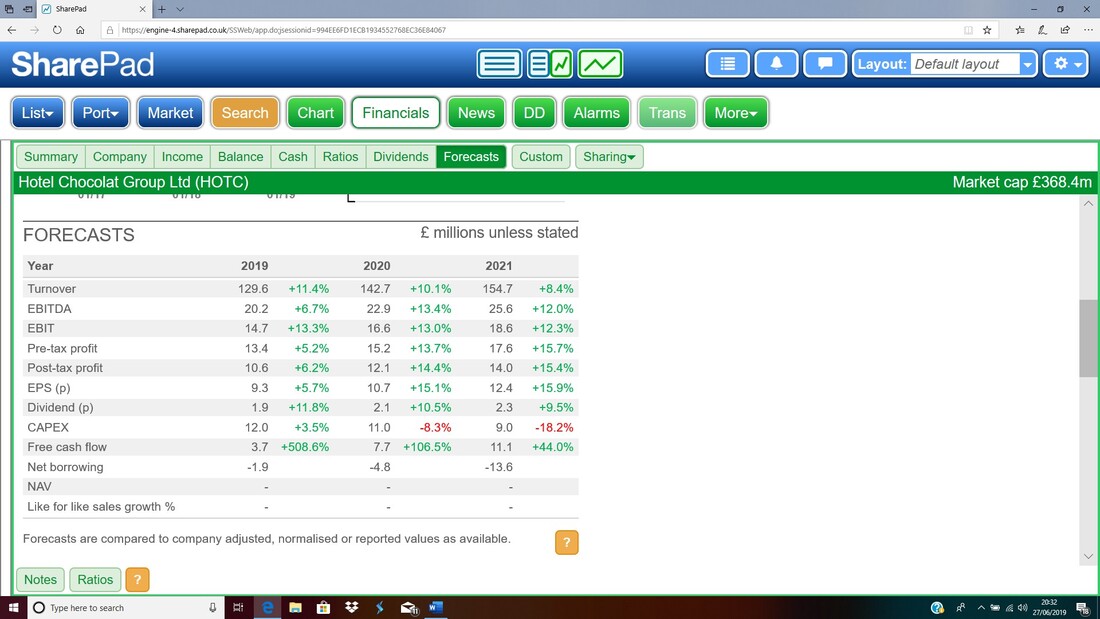

Valuation I have taken the image below from SharePad and I have zoomed in to try to make the numbers in the table on the left-hand side larger. If you click on the image it should get larger as well.

At the time of creating this Blog, the Share Price for HOTC is 326p and if we take the Forecast EPS (Earnings per Share) for 2019 (the current financial year) of 9.3p this gives us a Forward P/E Ratio of 35 (326 divided by 9.3) which is obviously quite a high rating. If we take the 2020 Forecast EPS of 10.7p then we get a 2-year Forward P/E of 30.5 (still a high rating but coming down if the Forecasts are met).

From a quick ‘sense check’ of the Forecasts the expected growth in Revenue over the Forecast period in the table and also for Profit before Tax and EPS look believable although there has to be some doubt around these and if anything they do look on the high side. Of course, if the expansion overseas works out then perhaps there is some upside or at least it could support these growth assumptions but again there has to be doubt around this. Bearing all that in mind, the nub really is around whether or not HOTC can keep growing and extending the success it has clearly demonstrated for many, many years and my expectation is that it can and will. If this occurs, then all we need is for the P/E Rating to remain the same and the Share Price can keep going up. To illustrate this point, lets take the Forecast P/E for 2019 of 35 and then project that forward for the EPS that is expected in 2020 of 10.7p (this is a theoretical exercise to demonstrate what happens if the rating stays constant so let’s assume the Forecasts are met) and we then get a new Share Price of 374p (10.7 x 35). If we then again keep the P/E rating at 35 and imagine the EPS has grown to the 2021 Forecast of 12.4p, then we get a Share Price of 434p (12.5 x 35). So this should show how a Share Price can grow without a re-rating of the P/E Ratio but of course it comes with risk along the lines that the Forecasts may not be met and the Market may fall out of love with HOTC and not give it the very high P/E Ratio it currently enjoys. Of course, on the flipside it is possible that the Forecasts are beaten and in that case it would mean that the P/E Ratio is artificially high and we would see the Share Price rise most likely and the Brokers would upgrade their Forecasts. It is of course a matter of personal taste and for me I think the risks around the high P/E are worth taking and can be mitigated by not buying too many Shares of HOTC and getting too heavy a Position. If I do get around to buying some HOTC, I will probably just buy a small Position initially (perhaps 1 to 2% of my Portfolio) and if the Shares fall back on a re-rating, and assuming there are no material problems within the business, then I might buy more and ‘Average Down’. I certainly see HOTC as something I could buy and hold for a long time and I expect the steady growth to continue. Another thing to consider is that HOTC in its last Interim Results had £21.8m Cash at the end of December 2018 and it is legitimate to subtract this from the Market Cap to calculate the P/E Ratio (the Market Cap divided by the Profit gives the same result as the Share Price divided by the EPS) and this would mean that the true P/E Ratio is actually lower than it appears. This method is using the ‘Enterprise Value’ for the Company and when it has Cash you subtract that from the Market Cap and when it has Debt then you add it to the Market Cap and then work out the P/E Ratio. This is a very valid method because it in effect helps the Valuation on Cash-rich Companies with a strong Balance Sheet and it punishes those with a weak Balance Sheet (by giving a higher P/E than you would otherwise get). I will let you perform these calculations !! I must just mention that this is not really a Stock that is likely to reward Shareholders much in terms of a Dividend at the moment. As you can see from the table of Forecasts, the expected Dividend payouts are miniscule and whilst the Company is in growth mode it is likely that Cash will be used to help expansion. However, as I just mentioned HOTC does have a fair bit of Cash on its Balance Sheet and this is gradually increasing so it is possible that we might see a Special Dividend in the future but I would not be buying HOTC for such a possibility. If it were to happen it would be a nice bonus. Targets This is quite a difficult Section to complete as it really depends on the timeframe we are considering. As I mentioned above in the ‘Valuation’ Section, if the P/E was to stay stable and the Forecasts are hit then I can see the HOTC Share Price hitting 434p in a couple of years (33% upside on the current Share Price of 326p) and I would anticipate seeing perhaps up around 500p if I can be patient. However, of course there are downside risks and upside risks to such Targets and things could play out very differently and the Investment Case really hangs on my judgement that HOTC is a high quality business with a very solid track record of achievement and it is this clearly demonstrated growth and the likely future trajectory that has got me interested. On the subject of future potential, HOTC currently has 118 Stores in the UK & Ireland and is targeting 200 in total, although it is not clear to me over what timeframe, but this does suggest that they can keep adding Stores for a while and these will help drive Revenue and Profit growth (although of course there are risks that come along with such a Rollout strategy). Last year HOTC opened 14 new Stores in this region so the 200 target leaves several years of growth from this source at that kind of rate. Technical Picture As always it is good practice to look at the ‘Big Picture’ first but because HOTC only listed in recent years, there is not a huge amount of Price History. My Chart below therefore goes back about 3 years or so and there is Support underneath from the Black Line with the Black Arrow and this implies that a drop below about 250p (which was hit back at the end of December 2018) would be a concern and suggest more falls. From where the Price is now, if it pulls back to the Black Line, then it should bounce at about 275p or so. To the upside my Red Horizontal Line (marked by the Red Arrow) marks All Time High Resistance at 405p. If the Price was to breakout above this then that would be very bullish. There is of course a bit of a ‘Flat-Top Triangle’ here with the Black Line at the bottom squeezing up towards the Red Line at the top – it will take time but if things keep going ok in the business then perhaps the Triangle will squeeze the Price to a Breakout of the Red Line.

On my next Chart I have zoomed in a lot so we only have the Price Candles going back for pretty much 2019 so far. First off note the Green Parallel Lines which are pointing out a Downtrend Channel which seems to be driving the Price at the moment – to go higher it needs to breakout of the upper Green Line.

My Black Arrow is pointing to a Hammer Candle which was created on the 18th June 2019 which is interesting because it bounced off the 200 Day Moving Average which is the Light Blue Wavy Line. My Blue Arrow is pointing to a Bullish ‘Golden Cross’ between the 50 Day and 200 Day Moving Averages but to be honest I don’t find these all that great an indicator.

My final Chart has a Blue Arrow which is pointing to a Bearish Cross between the Black Wavy Line which is the 13 Day Exponential Moving Average and the Red Wavy Line which is the 21 Day EMA (these are similar to Simple Moving Averages but they put more weight on recent Prices). These are an excellent Indicator and rapidly becoming my favourite for pretty much any Asset – the Signals they give are clear and once you get a Bullish or Bearish Cross, then it does tend to play out that way for a while. If you look at the Chart you can see what has happened in the recent past when such Bearish Crosses have been given etc.

What this is really telling us is that there is little point in buying until we get a Bullish Cross on these EMA Lines.

Conclusion

I’m really pleased I decided to produce this Blog on HOTC as it is a very appealing business and the process of creating the Blog has built structure and discipline into my digging into the Stock. I have in mind another Stock I am interested in and perhaps after scribbling something about Live Company Group LVCG I will do that one so I understand the Company better. As with HOTC I am in no rush to buy anything much at the moment but doing these Research Blogs well in advance gives me plenty of time to plan my moves (if you have been reading my stuff for a while, you have probably picked up that I never make quick, snap, decisions). The Market in general is not in the best of moods and with Brexit not far off and the potential for trauma that represents (particularly if we get a ‘No Deal’ outcome), I am happy to keep my powder dry and wait for things to play out. I bought some LVCG recently but it was a miniscule position just to ‘get my foot in the door’ (because if I don’t do this I will get distracted by some other Stock which winks at me in an alluring fashion). The big standout attraction of HOTC for me is its track record which as I wrote in Part 1, shows a very impressive progression in terms of Company size and its achievements year by year since formation around 26 years ago. It appears that the Management are very capable and the Founders are still there which I like and the CEO Angus Thirlwell is not all that old so the likelihood is that he hangs around for a good while yet. The moves towards more overseas locations are very interesting but of course they bring along risk. I think HOTC has quite a unique offer and has a certain ‘moatiness’ which comes from its history and Premium products. Customer loyalty is also very much a strong point. Of course, the big negative is the Valuation which is by no means a steal. As I have written in the ‘Valuation’ section above, if the Company keeps on growing (the track record so far suggests it should but of course all runs of achievement come to a stumble at some point in time) then the Valuation will be less of an issue but if there is trouble, then the Shares could get smashed. However, I think the way to manage this Risk is to build a Position steadily over time and to not get too heavily exposed at silly Prices. If I do take the plunge and buy some, I will probably only buy a maximum of 2% of my Portfolio initially and any sizeable pullbacks might be the chance to buy more at a better Price. I see HOTC as something of very high quality that I could hold for a long time and let the choppy seas of the Markets toss it about and not worry too much. There is also a possibility that it gets taken-over although the Founders would probably want a very high Price. One thing that has slightly crossed my mind is how HOTC has some similarities to Patisserie Valerie which I got heavily caught out on when the Accounting Fraud came to light (one other similarity is that on CAKE I wrote a detailed Blog well in advance of buying some Stock but that didn’t work out too well !!). However, this is just me being silly (although of course we must not forget expensive lessons from the past but in this case I do not foresee any trouble) and I will not let it put me off. Regards, WD. P.S., if you keep going into HOTC for the Free Samples then you best get a good disguise because they will suss you out !!!

0 Comments

Leave a Reply. |

'Educational' WheelieBlogsWelcome to my Educational Blog Page - I have another 'Stocks & Markets' Blog Page which you can access via a Button on the top of the Homepage. Archives

May 2024

Categories

All

Please see the Full Range of Book Ideas in Wheelie's Bookshop.

|