|

educational blogs |

|

Sheesh, where did that year go? I vividly remember last year when I wrote ‘Scores on the Doors 2014’ after I had had my worst year for ages - typically just after I had started doing the WD Website and stuff and it was a pretty sobering experience (don’t worry, I have been on the Hobgoblin so I should be suitably squiffy to write tonight !!). It was a huge credit to so many of my Twitter Followers who were really understanding about my dire performance and I thank you all again for your continued faith in me.

Fortunately this year the SOTD is so much easier to write as overall my Performance has been very strong. However, before I get too cocky, my Spreadbet performance is frankly disgusting and I need to address this over 2016 - and I suppose I need to do this reasonably quickly. It annoys me because I am just peeing Cash down the drain that I could so easily be scooping up - it has costs me many £Thousands (if not more !!).

I will go through each of my Portfolios (you can see these on my ‘Portfolios’ Webpage, surprisingly enough) and give details on the performance and any related thoughts.

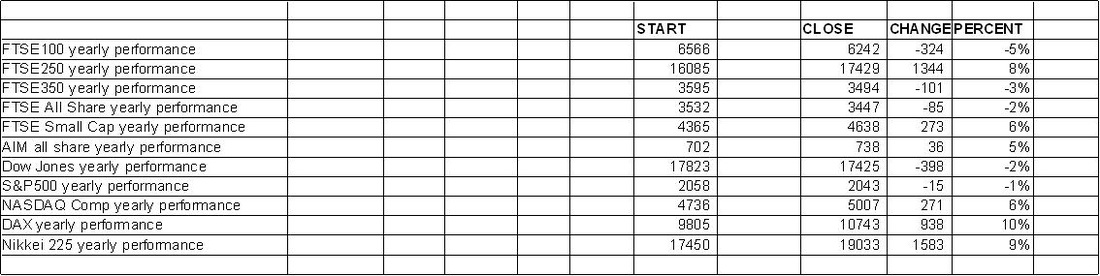

Indexes To set the scene, here is a Screenshot of how the Major Indexes turned out for 2015 - these are not including Dividends (i.e. they are not ‘Total Return’) and I calculated these myself from ShareScope numbers put in a Spreadsheet. They may not be Total Return but I guess in some ways they are fair Benchmarks as of course our Portfolios get hit by Dealing Costs, so in reality we could never really match the Benchmarks even if we bought exactly the same Stocks in the same Weightings. Roughly speaking, you can add on about 4% for FTSE100 Divvys and about 2.5% for the FTSE250. Isn’t it interesting how all the usual Media Suspects are talking about how badly the FTSE100 has done, when in fact it is only down about 1% on a Total Return basis……..

If you want an accurate Total Return figure, check out this link from @compoundincome (this is a Website that is worth visiting regularly, Jamie knows his sh*t):

http://www.compoundincome.org/blog/year-end-timing-indicators-cis-portfolio-review Trading ISA Portfolio Well, I am starting with this one because it has been so damned good this year, with a gain of 28% over 2015, after all Costs and including Dividends and obviously loads of reinvestment over the year as I bought new Stocks or added to existing Holdings - and of course Stocks that I sold had the money reinvested in something else. This is my biggest Portfolio so has a huge impact on my Wealth so I am really pleased. OK, I can whinge because I really thought I could hit 30% and it got very close, but a few duff days at the end of December meant I couldn’t quite get there. Overall I have been very pleased with how I have done here this year - areas for improvement are really around even better Stockpicking and concentrating on timing issues of Entry and Exit. I need to get to the WD40 as I go on about continually, but I will not sell stuff just for the sake of it. As I will explore further down, this Portfolio is critical as it should drive the performance of my Spreadbetting Portfolio - sadly this has not happened well this year, but the fault does not lie with my Trading ISA. As a general point, I am overall very pleased with the Stocks I have bought this year, and with just the odd few like TCM and UTW which have disappointed, I have had some really big Winners. I expect more gains from my Winners and the underperformers will most likely deliver the goods with patience. I am pretty much happy with my Stocks with the odd exception like FCCN which I really don’t like - I screwed up here in many ways (one was not selling out fast enough once I had decided it was not good enough for my Collection). Unit Trusts My small collection of Overseas Unit Trusts was up 9% in 2015. Although compared to my Trading ISA this is a bit flabby, in reality I am happy enough. I don’t expect amazing results here and it is very much a ‘buy, Hold and Forget’ Portfolio. I think a lot of the performance is driven by FOREX with US Dollar strength being a key factor - this is something I am unhappy with and over time I have been reducing the Money I have invested in these Unit Trusts - this is also because I think I can make better Returns investing the money myself in my Trading ISA. On the flipside, this Portfolio adds to my overall Diversification (a rare ‘Free Lunch’ that should be taken advantage of and all Investors can do this) and this makes me keen to keep it going but I just feel a need to amend it a bit. Here is the first of a series of Blogs I wrote recently which looked at this issue - the Conclusion was that I need to sell my European Unit Trust (or perhaps sell half of it) - I am still not 100% there with the Decision but it is likely that I will sell it very soon so I can boost my Cash reserves a bit and reduce my number of Holdings. If we get a bit of a run up early in the year, this would be a good rise to sell into: http://wheeliedealer.weebly.com/blog/diversification-am-i-enjoying-too-much-of-a-good-thing-part-1-of-3 Income Portfolio Right, this one is a bit harder to measure. In fact, it is so hard to measure the performance that I really can’t be bothered to do it !! Sloppy I know, but I have better things to do. The problem is that I have been adding Cash to the Portfolio throughout 2015 so it is not easy to do a proper Annualised Return figure. I could use the XIRR function on Microsoft Excel but I really have no enthusiasm to do this. The purpose of this Portfolio is to create a Dividend ‘Revenue’ Stream for myself so that in about 9 years when I hit 60 (yes, I am a shade off 51 - where did that year evaporate to?), if I want to, I can just take the Divvy Cash and spend it for a big part of my usual living Costs (more on these further down). In the meantime I am reinvesting the Divvy Cash whenever I buy a new Position or topup on an existing Holding - although I am not doing a DRIP (Dividend Reinvestment Programme) as I think they are a cr*p idea). On this basis, the Yearly Performance of the overall Portfolio is less important to me - what matters is the growth of the Dividend Stream. The Income Portfolio also has a benefit of diversification - more and more I find I am doing less stuff with FTSE100 type Stocks in my Trading ISA (mainly because I generally do much better on Smaller Cap Stocks) and this Income Portfolio therefore gives me diversification across Stock Size. In the absence of proper Return figures, let me just put down some simple Numbers from the Portfolio for this year:

Spreadbetting Account OK, this is where things start to go horribly wrong. The Value of my igIndex Spreadbetting Account increased by 38% - this may appear good, but due to Leverage this is truly awful and I am kicking myself hard (not easy with paralysed legs but it shows you how irritated I am by this !!). In theory, I am supposed to ‘Mirror’ my Trading ISA by using Spreadbets in similar proportions and I have clearly failed at this miserably. Let me explain this with an example:

Hopefully that should demonstrate the problem - 38% is actually woeful, pathetic !! In fact, it is worse. I did some Hedging during the Year and I made at least 0.75% (against my Total Exposure) on a FTSE100 Long Santa Rally trade - these probably add up to about another 30% on the Performance. Therefore, if you strip this out, my Mirror Spreadbet Portfolio was barely up at all !! Remember, Spreadbets are Leveraged and therefore very Dangerous - many people get into serious trouble (like losing House !!) with these things. This is partly why 38% Return is not acceptable - it is not enough to compensate for the Risks involved. A minimum I would be happy with is about 50% per year. Why did this happen? Obviously I need to sort this out as it is Cash being wasted and I am a total muppet for not addressing this earlier (I have been aware of the problem but not really done much about it). The underlying reasons I think are as follows:

If you click on the ‘Spreadbetting’ category on my Blog Page, then you can find loads of stuff on how to Spreadbet safely - but I do not recommend Spreadbets for beginners and it is best to start small. Prudential With Profits Bond I must just mention this Unsung Hero of my Overall Portfolio (I have not included this in my overall Stockmarket Returns in the Conclusion bit), this returned 7% on the Year which is superb and unexpected. I always think it will do 3% to 4% so this is really welcome. I have about 10% off all my Wealth in it and it really is a ‘Core Holding‘, so it had quite a nice impact. It’s a funny old beast. These are the things that get linked to Endowment Policies and they therefore have a bad name. However, mine is a standalone thing that I have had for about 16 years and it is pretty steady and solid. It came under some slight pressure during the Credit Crunch but it was nothing compared to what other Asset Classes suffered. I have been very pleased with this and it has some Tax Advantages. It is a ‘buy and Forget’ type of investment and I recommend it to anyone. I used to have one with Liverpool & Victoria (now LV= or some dopey name) but this one was rubbish - if you are tempted then go with the Pru. When I started Investing seriously in 1999 or so, this was probably my only good decision !! Only caveat here is that the 7% growth figure is calculated from the Last Paper Statement I received which was back in April - so it really represents gains from 2014 to a large extent. I am sure if I contacted Prudential they would give me the current figure - but not worth the bother. I always record it this way every year, so it is consistent and understates the true Value now. Ah, good old Conservative Accounting……. (If you recognise the text above, it is because I copied it from last year’s ‘Scores on the Doors’ and tweaked it a bit. Note, this ‘With Profits Fund’ has now made 7% for 2 years on the trot - flippin’ impressive). My Mate’s Unit Trust Portfolio If you go to the ‘Funds’ Page of my Website, you will see an Example Portfolio there which I run with a mate. This year that Portfolio was up 3% and we are a bit disappointed with it. Seems like the Bond Funds have not really compensated for weakness in the Equity element - we will be meeting in the coming weeks to do an autopsy on this and we need to do some rebalancing as my mate wants to take out some Cash for a House Extension. I keep saying they should invest directly in Stocks themselves !! Another Mate’s SIPP Portfolio I have another friend who copies my Trades in her SIPP (obviously no Readers should copy my Trades - please see Disclaimer on Homepage) and this year it is up 22%. Over a few years it is averaging 15% a Year which we are really pleased with - I always say we should be targeting 10% a Year compounded - so this is going very nicely. It is worth nothing how 2 people can have similar Stocks but quite different Results - in this case it is partly due to different Weightings and also because she holds some Stocks that I have in my Income Portfolio - so she has a bit of a hybrid Portfolio really. I also said she should sell RR. right near the peak some years ago but she was totally in love with it and held on while I banked a lovely profit - the rest, as they say, is history……(if you’re reading this, sorry !!) Overall Wealth After my 6th year of Retirement and Freedom (try it, it‘s marvellous), I have managed to increase my Wealth by 10% over the year - this is despite having a nice Cash Pile and some less well performing Assets. I am very pleased with this. Spending Really surprised by this - over 2015 I only spent £17,353 on ‘Living Expenses’ which was down 6% on the £18,378 I spent in 2014. Not really sure why this is, I guess being an Old Git my Car Insurance has dropped a bit but seems like lots of other costs, like Rent, Car Tax, have increased. Weird. I guess I save on Petrol (because I never seem to drive anywhere much these days !!) and since doing WheelieDealer I am probably perched in front of a Screen a lot more and not out spending Money. I don’t have expensive Holidays (this is really down to the physical limitations of being Paraplegic - in all honesty going away just means hassle for me) and I don’t smoke or anything like that. On the flip side, I run 2 cars but I do such little mileage that they never seem to need much repair work and suchlike (although a Rear Suspension Spring did break on the Leon hitting me for £350 - ouch !!). My Rent was £6576 this year, so if you strip this out for Reader Comparison purposes, my Living Expenses excluding Rent were £10,777. I could probably reduce this figure a bit by only having one Car. Obviously I am no big spender, but it is amazing how little I live on - means more Cash to invest - hurrah !! Conclusion No point me downplaying this, it is a very strong result and I am very happy. Sadly it is not my best ever year (I achieved this back in 2013 when I did 32% in my Trading ISA and my Spreadbet Portfolio was superb) but it is pretty damned decent. You know my irritation over the Spreadbet Account and this must be addressed, but 20% Return against the Capital Employed across all my Stockmarket Activities is lovely. This game is all about Compounding Returns over years - for instance, if you can grow at 10% a year then your Money doubles in 7 years. If you can grow at 15% a year, then your Money doubles in just under 5 years. Most people do not get this - it is utterly vital to understand and it really is one of the rare Stockmarket ‘Free Lunches’ - anyone can grab it so make sure you do. Something I just want to mention is that one of the most common discussions we have on Twitter on a regular basis is around how many Stocks to hold. What is interesting here is that despite having a huge number of Stocks, my Returns are pretty good - in fact, better than many from people with smaller, more focused, Portfolios. My suspicion is that the Risk Reduction benefits of having a wider and more Diversified Portfolio outweigh the supposed advantages of a focused Portfolio - interesting stuff. I would contend that I make pretty good Returns with a reasonable amount of Risk - people with focused Portfolios are taking on more Risk and really should be achieving far higher Returns to compensate - that’s got you thinking !! A strange thing about this Investing malarkey is that I always find there is room to improve and I can hopefully do better in the future if I make some changes - maybe this is a big part of the attraction and why I enjoy it so much - you never stop learning and improving. All in all, a very good year, let’s hope we can all do better in 2016 and good luck to all Readers !!! Cheers, WD. Related Blog Links Here are 2 Blogs on the subject of Compounding - to capture this effect you must keep your Risk low and make sure you don’t Crash the Plane - volatile Returns over the years will not help you - aim for consistency year in, year out: http://wheeliedealer.weebly.com/blog/why-bother-investing-the-power-of-compounding http://wheeliedealer.weebly.com/blog/the-rule-of-72-and-its-implications-on-our-expectations

10 Comments

Blue

4/1/2016 04:08:07 am

Fabulous, #WD..very well played...

WheelieDealer

5/1/2016 09:59:42 pm

Hi Blue, Thanks for the comments and for our ongoing discussions via Tweets etc. through the year - it's been good fun and so useful. As you say, here's to another good year on the Markets for us !!

Steve Holdsworth

4/1/2016 12:24:22 pm

A fascinating blog, Wheelie, and very honest too. I wish my performance in 2015 had been anything like as good!

WheelieDealer

5/1/2016 10:01:38 pm

Hi Steve, pleased you found it enthralling !! I certainly had a good year, and with luck we can keep this up. Maybe one day I will be brave enough to take on the XIRR......

Steve Markus

4/1/2016 03:20:09 pm

Very good WD, impressive performance. I remember 2013 as being a brilliant year, think I did about the same as you that year i.e 30% or so. This year returns have been a bit more pedestrian, more like 10% or so, but I am more than happy with that. Keep up the good work!

WheelieDealer

5/1/2016 10:04:35 pm

Hi Steve, thanks for the comments - I am obviously happy with the results this year overall. I remember 2013 being quite easy and the cash just flowed in - 2015 felt pretty like hard work so it makes it even nicer to have a good result. As you know, 10% Annually Compounded is my target so I reckon you gotta be pleased with your outcome - these things are quite variable over the years anyway.

dean

5/1/2016 07:06:34 am

Nice blog wd. Like the bit on living costs. Well done mate

WheelieDealer

5/1/2016 10:06:35 pm

Hi Dean - thanks for the feedback. It's funny, several people have mentioned to me that they like the details on the Living Costs - hopefully for people who are looking for Freedom it gives a bit of a steer as to what kind of Spending they may face.

dave diamond

6/1/2016 04:58:24 pm

Yep you're definitely the "normal" one well done matey id love that sot of return maybe I should start following you more closely Happy New Year !

WheelieDealer

8/1/2016 11:10:04 pm

Hi Dave, thanks for your comments - it's rare I get called 'normal'. Not a bad year for me but I am fairly sure anyone can make pretty good Returns if we follow some fairly simple 'Rules' like Running Winners, stop catching falling knives and avoid WheelieBin Junk. It is when we stray and lose our discipline that Returns get hurt. I would love it if you did 'follow me more closely', at least I would then konw I had 1 Reader !! Leave a Reply. |

'Educational' WheelieBlogsWelcome to my Educational Blog Page - I have another 'Stocks & Markets' Blog Page which you can access via a Button on the top of the Homepage. Archives

January 2021

Categories

All

Please see the Full Range of Book Ideas in Wheelie's Bookshop.

|