|

educational blogs |

|

THIS IS NOT A TIP OR RECOMMENDATION. I AM NOT A TIPSTER. PLEASE DO YOUR OWN RESEARCH. PLEASE READ THE DISCLAIMER ON THE HOME PAGE OF MY WEBSITE. IF YOU COPY MY TRADES, YOU WILL PROBABLY LOSE MONEY.

If you’re keeping up with the tinkering I have been doing to the WD Portfolio, you may remember I bought a small stake in Devro DVO some weeks back after they had a Profit Warning and the Shares had dropped a lot. This was quite unusual for me as I tend not to buy into ‘Trouble’ if I can avoid it - however, in this case, DVO is a Stock I have dabbled with in the past and I know the Company reasonably well. My logic here was that this could be a decent chance to buy into them at a good price and I was particularly interested in the increased Capacity that the new factories have brought along and how this could give them space to grow in the future.

Because I knew the Risk in buying a troubled situation, I only put 1% of my Portfolio Value into DVO as I am all too aware that Profit Warnings rarely come on their own and that they often come in 3s !! So, as Bad Luck would have it, this week DVO put out the obligatory Second Profit Warning, and the Shares duly tanked.

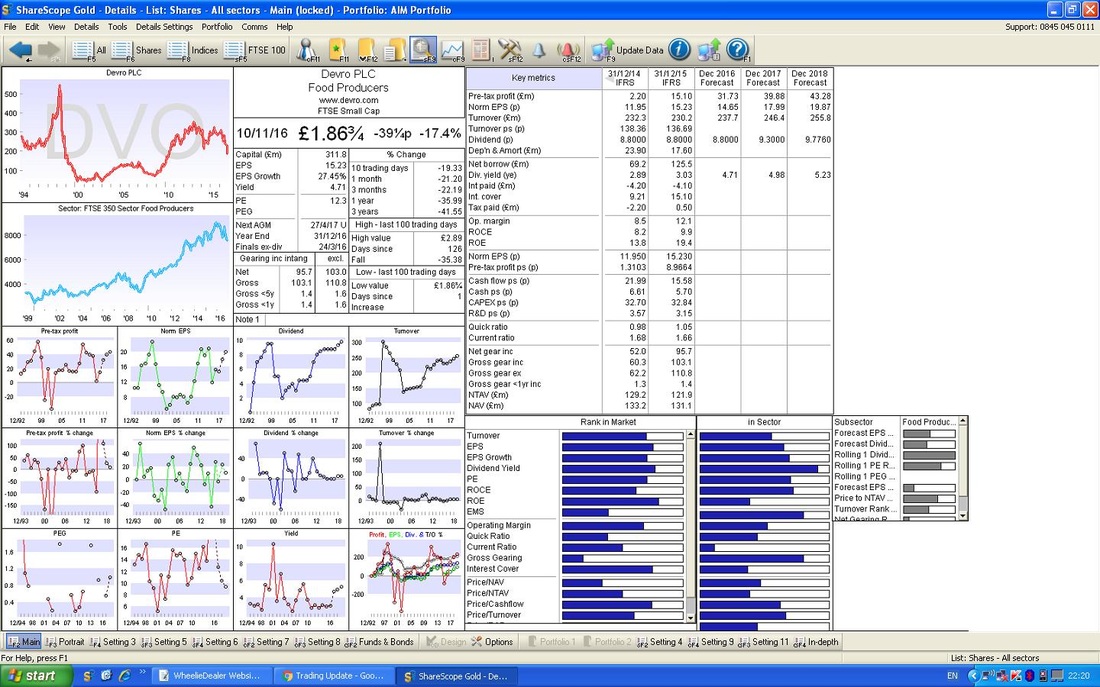

Following this latest bit of Bad News, I have seen various bits of speculation about their Debt Position, ability to maintain a Dividend and even the potential for a Breach of Debt Covenants (thanks to @shauniekent for highlighting this on Tweets) - so I thought it would be an extremely good idea to carefully dissect the Trading Update and crunch the Numbers to see what the likely Debt situation really is. When I set out on this task I assumed I would be digging deep into the Accounts to figure out how the Numbers would look in the new scenario of falling Sales and Profits - however, during my digging I tripped over a simple and straightforward way that I could assess the Debt Covenants issue and I cover this at the end. Despite all the Trading Issues, the Debt Covenants is the really critical bit. The Profit Warning The offending update came out on 10th November 2016 and you can read the full thing here. For the purposes of this Blog, I will hack it about and address the bits that I think are of importance: http://otp.investis.com/clients/uk/devro_plc/rns/regulatory-story.aspx?cid=1810&newsid=816224 “Sales volume trends were broadly similar to those experienced in the first half, enhanced by improvements in Russia and South East Asia, but impacted by further reductions in Latin America due to the previously highlighted issues, which are being addressed, related to the transformation of our global manufacturing footprint. Combined, these factors have had an adverse impact on margins, offset by further benefits from lower input costs and foreign exchange. As a result, the Board's full year expectations for underlying operating profit* remain unchanged.” Obviously it is good to see Russia and South East Asia improving in terms of Sales Volumes - however, note the word ‘Volumes’, this makes me wonder if the number of Sausage Skins being sold is the same but perhaps they are selling them for lower Prices so the Monetary Value of those Skins sold might be less. They then go on to mention trouble in Latin America and talk about “an adverse impact on margins” which goes exactly to my point about the selling Prices being lower. However, this Margin squeeze is then mitigated by Cost reductions and benefits from the weak Pound. On the positive side, it does say they are addressing the issues. “Our new factories in the US and China are now integrated into the Group's manufacturing base, completing the transformation of our global manufacturing footprint. As expected, in the second half £8 million of exceptional costs related to these capital investment projects have been incurred, including £1 million of additional foreign exchange movements. There will be no further exceptional costs related to these capital investment projects.” This is good news that the new US and China factories are integrated (whatever that really means !!) and they make a pretty confident statement here that the Exceptional Costs for the Second Half of this year from the Factories will be £8m. “Based on current trends, sales volumes in 2017 are now expected to be approximately 10% lower than previously anticipated, which will result in an under-utilisation of available capacity. Actions are being taken to rebalance the use of capacity across our global manufacturing base. The under-utilisation is expected to have a further adverse impact on margins.” Now they go on to 2017 and say that Sales VOLUMES will be about 10% lower than expected - but because Margins are impacted as they mention in the next sentence, I take this to mean that Sales VALUE will be worse than just a 10% hit - it might be perhaps 20% (who knows? It could be higher.) From consulting the ShareScope ‘Details’ Screen (if you scroll down this Blog to the bottom you can find an image of it which I captured a couple of days ago - it is still valid), the Broker Consensus Forecast for Sales in 2017 is £246.4m - so if we reduce this by 15% we get a figure around £209m (I have chosen 15% with an air of optimism for my Number Crunching purposes at this stage). Note the Turnover (Sales) Forecast for the Current Year is £237.7m, so my revised Sales figure for 2017 is about £29m less than that expected for this year. “The Board has decided to accelerate and implement more extensively the next stage of the Group's strategic development, focusing on growing sales through improved commercial capabilities, introducing the next generation of differentiated products, and further improving manufacturing efficiencies to reduce unit costs. This improvement project will deliver a fundamentally more competitive position. The benefits will offset the effects of the lower volumes, partially in 2017 and fully in 2018.” Now they get onto the action they are going to take to try to get a grip of things. Presumably “improved commercial capabilities” means a more focused/more efficient/bigger Sales Force but it is unclear. They then talk about New Products which sounds sensible and improving the efficiency of their Factories to lower costs - this makes sense and it is likely the lower cost base will make them more Price Competitive in future. They then imply that Sales Volumes are likely to remain lower in 2017 and 2018 than they currently are. I have to say I am a bit concerned about this - it is not really clear to me why the Sales Volumes are struggling so much - this should be a steadily growing market as Population grows and people in Developing Countries get a taste for meat as members of the Middle Classes - it should be a good tailwind for DVO. “Consequently, the Board now expects underlying operating profit* for 2017 to be lower than previous expectations. There will be additional costs and capital expenditure associated with the improvement project. Given the nature and scale of the planned actions, these costs will be charged as exceptional items, of which approximately £3 million is expected to be incurred in the final quarter of 2016.” This is the really really BAD NEWS - Underlying Operating Profit (before Exceptionals) will be hit in 2017 and then we have the impact of Exceptional Costs arising from the New Strategic Projects - so Profit Before Tax (PBT) is going to take quite a hit by the look of things. In the Current Year there will be an ADDITIONAL hit of £3m (so Debt will rise by this amount at least I expect) and because that is the Charge for 1 Quarter, it seems plausible to me that the full Exceptional Cost for 2017 is perhaps £12m (4 lots of £3m) - so this will hit Profits hard. “Devro's markets remain attractive. With completion of the capital investment projects the Group now has an excellent manufacturing base and, with the benefits resulting from the improvement project, the Board considers the Group to be well positioned to grow revenue and profits over the long term.” I need cheering up after all that, so now we can look a bit further out and dream about the Sunlit SausageSkin Uplands - as they state, their Markets should be attractive; they now have a much enhanced Manufacturing Footprint (it’s looking way too big at the moment !!); and they claim the wondrous new Projects will help them back into Sales and Profits growth in the Long Term. This is fair enough, but they need to get through the Short Term first. If I get really Rose-Tinted, all this extra Factory Space might be very attractive to one of their Competitors or perhaps a Private Equity outfit if the Shares get any cheaper. Where does this leave us? I now want to try and crunch some numbers and see how the Debt Situation looks after this exercise. Debt In the last Trading Update (see my previous Blog - there is a link at the bottom of this one) they said the following about the Debt: “As the three year investment programme comes to an end, net debt increased to £147 million at 30 June 2016 (or £153 million including derivative liabilities), compared with £126 million at year end 2015. This includes the effect of a significant weakening of sterling in June 2016 (given that a part of the group’s debt is denominated in US dollars) following the result of the EU Referendum vote on 23 June 2016, which increased the reported net debt figure at 30 June 2016 by approximately £15 million (including the effect on derivative liabilities).” From this, I take it that the Net Debt at the 30th June 2016 was £153m (I have taken the figure including the ‘derivative liabilities’ for the sake of prudence). This paragraph then highlights the issue that was being mentioned on Twitter about the Debt Covenants being in trouble because of Forex - as you can see the fall in Sterling had quite an impact on the Dollar Denominated Debt by the 30th June but since then Sterling has fallen further so this could be causing more problems. There is clearly an issue here. It is difficult to model how the Debt will have moved since the 30th June 2016, but as a start if I take the Net Debt figure of £153m and add on the £8m of Exceptional Costs from the US and China Factories and the £3m from the New Strategic Programme that hits this year, we get a Guesstimated Net Debt of £164m. It is very possible that this Guesstimated Net Debt figure actually understates things - but it is good enough for my purposes. But since 30th June Sterling has fallen a lot against the Dollar - from a Rate of about 1.35 down to about 1.25 today - a drop of nearly 17%. Keeping things simplistic, it seems fair to assume the impact on Debt of the further falls in Sterling since 30th June has had a similar impact - in other words it adds another £15m to the Debt - so we now get a Guesstimated Net Debt of £179m for the end of the Current Year. Debt Covenants I will now attempt to work out how this fits with the Debt Covenants - on the basis that the latest Trading Update says Operating Profit will remain unchanged but there will be an additional £3m Exceptional Cost. If they let us down on Operating Profit by Year End, then the situation would be worse. The following text comes from their last Results, and I have lifted it from my earlier Blog: “At 30 June 2016 the net debt to EBITDA ratio was 2.9 times and the EBITDA to net interest payable ratio was 9 times, meaning both ratios were within their limits (of <3.25 times and >4 times respectively) despite the recent changes in exchange rates. There will still be some cash outflow in the second half related to the transformation, both in terms of capital expenditure and exceptional items, but by the end of the year the Board expects the net debt to EBITDA covenant ratio to be lower than at 30 June 2016.” We know that at the 30th June 2016 the Net Debt was £153m, so if we substitute my Guesstimated Debt Figure of £179m, we get the following Ratio:

This clearly falls outside the <3.25 times Debt Covenant Limit - so there could be a problem here. It is highly possible my Guesstimated Net Debt figure is wrong but if anything it is most likely to be worse - it does look like they are either in Breach of this Debt Covenant or if not they are extremely close to it. In terms of the Net Interest Payable Ratio, on the basis of the Debt being £153m at the 30th June, by some Mathematical mucking about, the Interest Payable was roughly £5.9m (I haven’t dug into the Accounts to check this figure - for my Purposes I am happy to do it with rough numbers). If we assume the Debt increases from £153m to £179m (a rise of 17%) and we take another assumption that the Net Debt Interest rising by a similar amount, then the following Ratio applies:

This seems to be easily within the >4 times Debt Covenant Limit - this demonstrates the highly Cash Generative nature of this Business which has always been a big attraction for me. But of course remember that the situation could be a bit worse than this. Summary These are very rough assumptions but it is good enough to give me a view that I think DVO are in breach or very close to breaching the ‘Net debt to EBITDA ratio’ Covenant - in fact, the situation could be worse. Something that has occurred to me is that it looks like they can probably afford the increased Interest Charges as they are so Cash Generative - however, with Sales and Profits to be hit in coming years, it doesn’t look good. I would guess that DVO will have to cut their Dividend (probably remove it altogether until the Debt Situation improves) and it is possible they might need a Rights Issue if they cannot get their Banks to agree to relaxing the Covenants etc. Alternatively, rather than a Rights Issue that is open to all existing Shareholders, they might do a Placing to just Institutional Shareholders - this would be annoying perhaps but it is often the cheapest and easiest way for a Company in trouble to raise Capital and even after this I expect it would mark the Bottom in the Share Price. Exactly this has happened to Quantum Pharma QP. in recent weeks. I will just re-iterate that point - Stocks often recover from a troubled situation once there is a Rights Issue and/or Placing and if this is accompanied by a change of Directors then it can often be a good time to Buy. Obviously if these scenarios play out, I will be looking closely at DVO with regards to buying more and Averaging Down. In simple terms, my Investment in DVO is not going at all well and I will not be putting any more Money into it unless and until the Debt Situation is addressed and Trading takes a marked improvement. I am happy to hold my Small Position (I am so pleased I only dipped a toe into this one) until such a change takes place - in fact, if there is a Rights Issue at an attractive price then maybe I will take that up. There is of course a possibility that a Competitor or maybe Private Equity will snap them up, but the Debt situation is pretty ugly here so that may be unlikely really. In the meantime, it seems highly probable that the Share Price will continue to drift downwards - but of course we don’t know when a Rights Issue or other similar solution will be announced so the Shares could bounce very quickly. Thankfully my small Position means it has little impact on my overall Portfolio even if it drops lower from here. Serves me right for Buying Trouble……….. Cheers, WD. P.S. Don’t blame me for the Title of this Blog - that was all @ExPatDealer’s Evil Genius…. Exhibit 1 - ShareScope ‘Details’ Screen

Related Blog

You can read a detailed Blog I did on DVO a while back here - this should give you a pretty good background on the Business and the Risks/Attractions: http://wheeliedealer.weebly.com/blog/devro-dvo-is-there-dosh-in-sausage-condoms

0 Comments

Leave a Reply. |

'Educational' WheelieBlogsWelcome to my Educational Blog Page - I have another 'Stocks & Markets' Blog Page which you can access via a Button on the top of the Homepage. Archives

May 2024

Categories

All

Please see the Full Range of Book Ideas in Wheelie's Bookshop.

|