|

educational blogs |

|

I am starting this Blog with a heavy heart because my Performance in 2018 was very poor (and that of my Portfolio for that matter !!). I am sure Readers can imagine how it goes where after a good Year I am enthusiastic and eager to get this Blog written but in rubbish Years it truly is a chore that I would rather not have to do !!

But of course that is silly talk and it is vitally important to stay calm and robotic and like I say on so many other aspects of Investing it is crucial to just go about the same things Day in and Day out and of course Week in and Week out and by the same manner, Year in Year out. So I will try to stay focused on the task and just get the information down on the page in a thorough and comprehensive way as I always do every Year. After all, it is just Numbers…….

I recently recorded a Twin Petes Investing (TPI) Podcast with Peter @Conkers3 and we discussed a lot of my Performance over 2018 and you might find it interesting to add more colour to what I have scribbled in this Blog. You can find it here and there is also a Link on the ‘Podcasts/Videos‘ page which is on WD2):

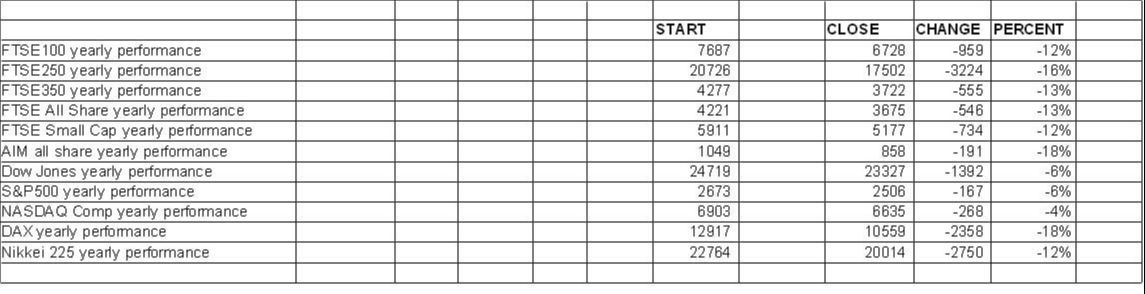

https://soundcloud.com/user-479955511 Indexes Here is a little table I bashed up using Excel and I took the Values for the Starting Numbers and the Finishing Numbers from SharePad. One thing that was a bit strange is that 2 of the Indexes had slightly different Starting Numbers to where they actually finished last Year - however, it is a tiny difference so I don’t think it is something to obsess about. In addition, please note these are just raw figures from the Opening and Closing Levels of the Year and they do not include Dividends. Obviously this depends on the Index and on something like the FTSE100 the Dividend Yield is a bit over 4% so a more accurate Return would be something like Minus 8% and the FTSE250 has a Dividend around 2% so that would be a Total Return of about Minus 14%. Perhaps the biggest surprise for me here was that the German DAX was down 18% and one of the worst of the Major Indexes - remarkably AIM managed a similar outcome !! It is also worth noting that the US Indexes faired much better but they did very well at the start of 2018 and then tailed off big time as we got near the end of 2018 - this meant that they had built a ‘Buffer’ of Gains in the early part of the Year which resulted in the much smaller Drop for the Full Year. However, the Drop from the Peaks in 2018 for the US Markets was much larger.

Trading ISA Portfolio (the WD40)

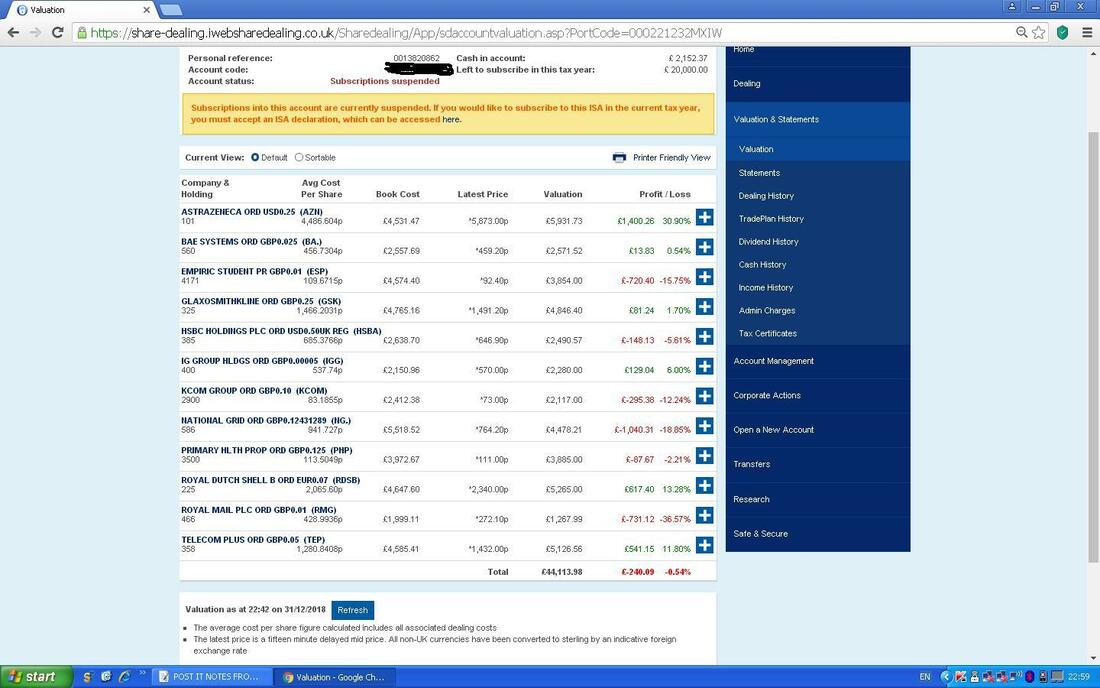

This is really where the bulk of my Money sits and sadly it had a very poor Year with it being down 13% but actually this understates the damage because I am holding Patisserie Valerie CAKE in this Portfolio and for ease of managing the Numbers I have just taken the Account Valuation at the end of the Year and compared it to the Start of the Year. CAKE is suspended at the moment and it is showing as the Full Value before the problems so it is not a true reflection by any means. I won’t know the actual picture until CAKE starts trading again and I expect it to tank so that would mean a hit of about 1.5% to my Account I would guess. It will also do a bit of damage to my Spreadbet Account because I have a Long Position on CAKE. Also please note that in the WD40 my Results include any Dividends received and Cash sat in the Account and also it allows for all Costs that were incurred on Dealing Fees and suchlike - not that I did many Trades over the Year. My WD40 Account really has a mix of Stock Sizes with stuff from right across the spectrum from the FTSE100 through the FTSE250 to Small Caps and AIM Stocks - so a blended comparison with the Index Returns would be appropriate. With the FTSE100 down 12% and the FTSE250 down 16% etc. maybe a Blended Figure of around 14% is about right. Bear in mind the effect of Dividends (my WD40 Account probably has a Dividend Yield around 3%) which would perhaps make a 12% Comparison figure about right, and I did very poorly because with Dividends I was probably down about 16%. Clearly a Year to put behind me as quickly as possible !! Overseas Unit Trusts For 2018 these gained 9% and I am assuming it was from 2 effects - partly a Forex thing with the Pound being weak in parts and probably more because the Nasdaq in particular did very well and I fortunately sold out of both the Unit Trusts I had (a Technology Fund and a Health Fund) a little while before the end of the Year so I missed the big drops on these. However, I did replace them with Investment Trusts in the form of Polar Capital Technology PCT and Worldwide Healthcare Trust WWH but I bought within my iDealing ISA Account and in smaller size (much smaller in the case of PCT). See my ‘Trades’ page for more details on these changes - they were partly because I prefer Investment Trusts to Unit Trusts but also to get my exposure here into an ISA Wrapper. I intend to buy more of both in the future. I also will count these within the WD40 so I have in effect increased my Concentration by doing this - so I now hold about 40 Stocks in my WD40 ISA and 12 Stocks in my Income Portfolio but there is also an ‘odd’ one which is Paypal PYPL which I only hold in my Spreadbet Account (having said that, on my ‘Portfolios’ Page I think this is actually included in the WD40). Income Portfolio I find a huge irony in the Result from this ’do nothing’ Portfolio - for more detail on this skip over to my ’Portfolios’ page and you should find it there. Anyway, the Portfolio gained 3% which in the context of the falls on my other Portfolios and in the Major Indexes, this is not a bad result at all. There is no doubt that much of it comes from the constant flow of Dividend Payments which I will go into in more detail in a mo and also the Portfolio has quite a Defensive slant. My Target Total Return on this Portfolio is 7% so I am way down on that this Year. In the 4 and a bit Years I have been running this Portfolio it is now up 30% on the Cash I originally shoved in (£38,670). It was very much a story whereby the gains earlier in the Year put the Portfolio in good stead when the difficult times came later in the Autumn and at one point the Portfolio was up nearly 10% but sadly it couldn’t hold this when the storms roared in (oh, the drama !!). The irony arises because I work my butt off on my ‘Normal’ Portfolio, the WD40, and focus all my efforts on that but the Portfolio which I barely even checked all year managed to outperform my WD40 by 16% or more !! And another thing to notice is that a couple of the Stocks I hold in the Income Portfolio (out of 12 in total) actually had Profit Warnings and got beat-up as a result. Of course the diversity paid off here and Stocks like AZN and TEP had very strong Years and that combined with the Dividend flows and the lack of Costs did a lot of the ‘easy’ work for me. I have added a Link to a Blog Series I wrote some time ago about how I go about my Income Portfolio and the things that need to be considered in order to set one up yourself. My intention is that as I get older and perhaps less able to ’work’ so hard on my Stocks, I will move more of my Dosh into an Income Portfolio kind of approach which is characterised by Low Risk, Low Effort, reasonable Returns, a constant flow of Cash and not much to worry about. Unlike my other Portfolios, I am happy to show actual Pound Note figures for my Income Portfolio and the ScreenShot below (you can click on it to see more detail) is taken from my iWeb Account and gives the Valuation along with the Breakdown for each Stock (but I must remember to use my new MS Paint ‘skills‘ to redact the Account Number !!). If you skip back to the ’Scores on the Doors’ Blog for 2017, then I included the same information in that one and you can compare if you are really so inclined. Note I have not added any Money to the Account over 2018 and I actually took out £4000 in Cash which I intend to shove back in there at some point soon so the true Total Valuation is £50,266. I normally reinvest Dividends that build up once they get to maybe £2500 to £3000 etc. and of course if I sell anything (it is rare but it has happened in the past and I think there have been 2 Takeovers in the few Years I have been doing this) I will reinvest that Money if I think the time is right. At the moment with all the shenanigans around Brexit and all that I am keeping my Powder dry but I am very keen to buy some Vodafone VOD as it pays a juicy Dividend and I think it has upside potential as well over time.

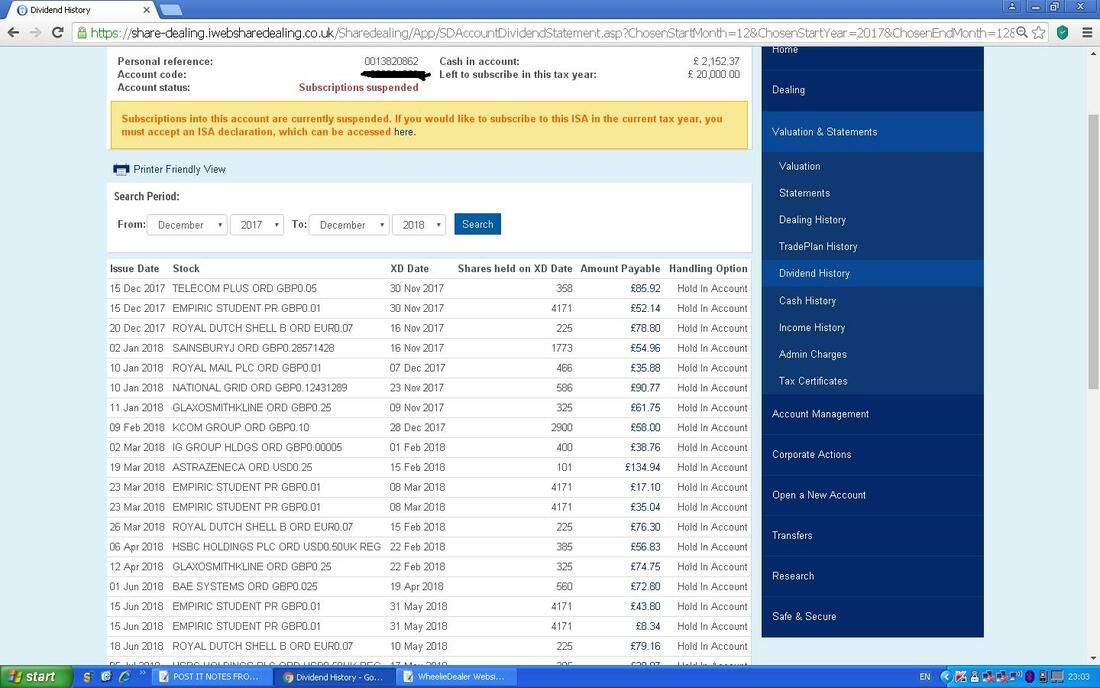

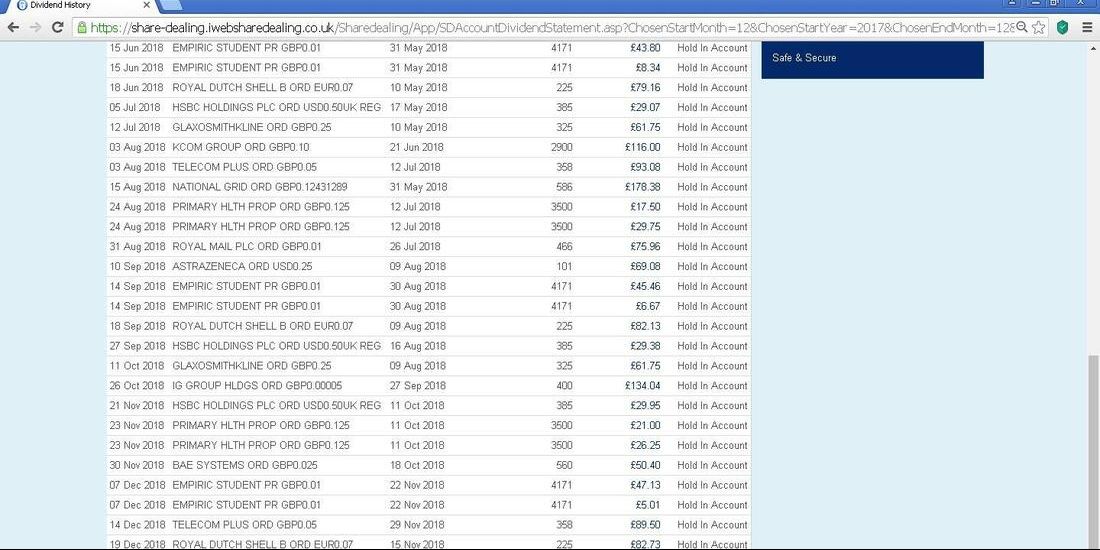

Just above I was going on about the flow of Dividends and the 2 ScreenShots below are capturing the Dividend Payments I received into my iWeb Account over 2018. As you should be able to see, I got some nice amounts of Cash every Month and it is quite impressive how the Cash steadily builds up and it doesn’t seem to take long before you have a nice pile of Cash ready to buy something with - either a new Stock maybe (my plan eventually is to push this up to 15 Stocks but that is the limit) or to buy more of a Stock I already hold.

If you add it all up together, the total Dividends received over 2018 were £2,321 but sadly this was down a lot on the 2017 figure of £2,904. I have not gone into detail to analyse why this was the case but my hunch is that last Year there was a Special Dividend from something (it might have been NG. I think) and I think KCOM cut its Dividend Payment this year - that was one of the Stocks that warned. Of course another factor could be that I had a fair chunk of Cash sat in the Account all Year which wasn’t generating Dividend Flows - this might have been as much as £200 or more that was missed out on. It is obviously important to get my Cash working for me but with the dodginess of the Markets I felt it was better to bide my time than risk the damage to Capital if I had invested the Cash only for the Stock to fall. In terms of Dividend Yield, the sum received this Year was 4.7% on the Starting Value on 1st January 2018; 6% on the Cash I put into the Account a few Years ago to get things going; and 4.6% on the Final Value at the end of 2018 (£50,266). My target is to get a 5% Dividend Yield on the Portfolio over a given Year so the Return of 4.7% is slightly below where I would ideally like to be. I need to monitor this over time and it might mean that at some point in the future I need to Sell a Stock that has run up well and consequently the Dividend Yield has dropped back a lot (AZN springs to mind) and then to replace it with something that pays a higher Dividend but obviously it needs to be a Quality Stock as well. Another action could be to Sell a Stock like KCOM that has been a bit troubled and to buy a Replacement with that Money - we shall see but I am not rushing into anything. At this point in time I do not need the Money that is generated from Dividends although perhaps in the future I will just stick my hands regularly into this Cash. Once I get to that stage it might be more important to keep the Dividend Yield % up at the 5% level but for now I am happy to let the Capital Gains element of decent Stocks like AZN continue to run up. At the bottom of this Blog I have put a Link to some Blogs I wrote that contain Checklists for Buying different types of Stocks and there is one that sets my Criteria for an Income Portfolio Stock.

Spreadbetting Account

A tough Year in my Spreadbet Account - but they always seem to be !! On the Starting Capital for 2018 the Account was Down 45% which looks a pretty horrendous figure but this is quite a false picture of what has actually happened. The reality is that the way I use my Spreadbet Account is mainly in order to ‘Leverage up’ my normal Shares Portfolio and in effect I ‘mirror’ my Normal Share Positions as Long Spreadbets. If you go to the bottom of this Blog there is a Link to a Blog Series I wrote all about Spreadbetting and this should make it clear how I do things. When you consider it in this way, the Return on the EXPOSURE in my Spreadbetting Account was Down 14% which actually seems quite consistent with a Portfolio of Spreadbets which mirror a Portfolio of Normal Shares. Obviously it cuts both ways because for 2018 a Drop of 14% on the Exposure has led to a 45% Drop in terms of the Capital Employed - this is the effect of using Leverage. And on the same basis, it wouldn’t take much of a rebound in my Long Positions to recoup a chunk of that Capital Loss pretty swiftly and this is in fact what has happened in the early Days of 2019. There are a couple more nuances to this. Firstly my understanding is that a mirrored Portfolio of Spreadbets will always underperform a Normal Share Portfolio by about 3% a Year or slightly more as a result of the Interest Charges you need to pay to cover the Finance Costs (see the Blog because I think I have covered this in it). And the other twist is that I did quite a lot of Index Trading over 2018 (see my ‘Trades’ Page for full details on all the Trades I did) which was characterised by a lot of Small Losing Trades and a few fairly Large Winning Trades. I am guessing that the Net Effect of these Trades was probably about Zero (a true geek could go through my Trades Page and work the Net Return out but I really can’t be doing with that !!) but I learnt a huge amount about Index Trading and in particular it has made me a lot more aware of the use of the 13/21 Day Exponential Moving Averages and how they can help me and it was worth the effort and the occasional frustration to learn these lessons. Another factor which I think influenced the Spreadbet Account Result was that my ‘mirroring’ is nowhere near perfect. For example, in my WD40 ISA, I held a big Position in ETO which did really well yet in the Spreadbet Portfolio it was relatively very small. In a similar vein, my Spreadbet Portfolio also held some ‘mirrors’ of my Income Portfolio Stocks - but only a few of them. Another difference was that I only hold PYPL in my Spreadbet Account and that did really well - so my WD40 ISA missed out on this gain. I have no doubt it would work better if my mirroring was more exact. As we speak I am using Short Spreadbets on both the FTSE100 and S&P500 in order to Hedge my Long Portfolios and I intend to use this approach a lot in the future when I think things are looking a bit iffy. My Mate’s Unit Trust Portfolio If you refer to the ‘Scores on the Doors’ Blogs I have written in past years, I have included a section which covers how my Mate’s Unit Trusts have done, but unfortunately this year I have not got an updated figure yet because she tracks it using what was the iii Website but that has now changed its policy and several of the Stocks she holds are not capable of being included in her ‘Virtual’ Portfolio. The intention is to help her sort this out when she has some time so once I have more news I will provide some sort of update which gives an idea of how her Portfolio did in 2018. My concern however is that we won’t get this done for a while so it might get a bit out of date. You can see what is in her Portfolio at the bottom of the ‘Funds’ page which I think sits on the WD2 Website (there is a Button on the Homepage of this main Website). Another Mate’s SIPP Portfolio This friend pretty much just copies my Trades but scales them down to suit her Portfolio size. Last year it was down 17.2% which is obviously very disappointing (for both of us !!) and a bit worse than my Portfolio which I am assuming is down to Position Sizes which differ a bit - particularly because I have quite a large Entertainment One ETO Position which helped my Portfolio as it had a decent year. Prudential ‘With Profits’ Bond Please note, for ease of producing this Blog, I have copied and pasted a lot of the Text below in this Section and just tweaked it a bit. Sorry if it rings bells with you from when you read it last year !! My Pru ’With Profits’ bond is up 8% on the Year which is really top notch especially when you consider the lack of effort (I do nothing to it all year - just pick up an Envelope off my Doormat around April and rip it open to see how it has done over the Year before) and with a very low Risk level it is pretty impressive. It is even more impressive when you consider that it was up 7% in 2017 - that is really decent. Having said that, I doubt the amount it gains in 2019 will be as good because they assign the ‘Bonus’ each year depending on how the overall Fund did and I suspect it found life tough like most of us did. In addition, 8% is the best Year I have ever had on it I think. I have about 15% of all my Wealth in it and it really is a ‘Core Holding’. Please note I get my Statement in April so there is a timing mismatch with when I do the Numbers for the rest of my Portfolios. I always record it this way every year, so it is consistent and understates the true Value at the moment. Ah, good old Conservative Accounting. However, I have now got an Online Account with them so I could check the Value at any time but for now I will just carry on as I have done for about 19 years !! (a true creature of habit). It’s a funny old beast. These are the things that get linked to ‘Endowment Policies’ and they therefore have a bad name. However, mine is a standalone thing that I have had for about 19 years and it is pretty steady and solid. It came under some slight pressure during the Credit Crunch but it was nothing compared to what other Asset Classes suffered. I have been very pleased with this and it has some Tax Advantages. It is a ‘buy and Forget’ type of investment and I recommend it to anyone. I used to have one with Liverpool & Victoria (now LV= or some dopey name) but that one was rubbish - the Pru one is defo the best. When I started Investing seriously in 1999 or so, this was probably my only good decision !! (and that was a lucky accident because my Parents used to invest in it…..) Overall Wealth Across all my Stockmarket Activities, I was down 14% on the Year - this is on the Capital used (not the Exposure which is of course a factor of Spreadbet Leverage and would actually be quite a bit better) and is across my Trading ISA, my Spreadbetting Account, my Overseas Unit Trusts and my Income Portfolio, but this does not include my Prudential With-Profits Bond which I think has a partial exposure to Stocks but due to the way they assign a smoothed ‘Bonus‘ Payment each year, it does not really behave like a Stockmarket Investment. Obviously this was a tough year for me and I could do without a repeat of this in 2019 etc. !! Spending Over 2018 I spent the princely sum of £16,996 on my ‘Living Expenses’ which was 2% up on the amount I blew in 2017 and still remarkably similar to the kind of figure I have been spending for each of the last 9 years or so that I have been ‘Retired’. This sum does not include the purchase of my new Car (which is a ‘one-off’ Expense obviously) but it does include a few small Costs related to the Car purchase which would be little things like a Steering Wheel Lock thing and a set of Halfords Mats (only to find out that the Car came with a set of ‘Cupra’ logo’d Mats but I have bagged them up and put them in storage for if and when I sell the Car in the distant future). I am very aware that several of my ongoing Expenses like Broadband, Electricity and Gas, Water Bill, Sky TV, etc. etc. have risen a bit and I really ought to address these and see if I can get them reduced - we shall see but of course a higher Charge now than I need to pay simply gets added to next year and following years and compounds the problem - I really must see what I can do to attend to this. Following a Motorcycle Accident in 1998 (blimey, 20 years has whizzed by in a flash !!) I am Paraplegic (paralysed from the Chest down in my case) and as a result I live in a Housing Association Bungalow on which I have an ‘Assured Tenancy for life’ and this suits me really well because if anything goes wrong then I just make a phone call and they fix it. Anyway, my Rent amounted to £6,397.03 which is down about 100 quid on the amount I paid in Rent last year - this is due to the Government trying to make life easier for the JAMs (Just about Managing…..) and they actually lowered my Rent which is remarkably unusual !! I also run 2 Cars although I don’t drive either of them all that much (I probably do about 4000 Miles a Year across the pair of them) and I could easily save money by getting rid of one of these, although I don’t think they really cost all that much in Servicing, Insurance and Tax etc. (note on my new Seat Leon Cupra I don’t pay any Car Tax because it is registered as a ‘Disabled Vehicle’ - with 290 BHP !! However, the Car Tax on the Z3 has been crawling up every year and it is getting near the point where it is more than my Insurance which is bonkers really but the 2.2 litre 6 Cylinder Motor is seen as being a polluting gas-guzzler). One great thing about getting my new Cupra is that because everything on it is new, I might get a grace period where I do not spend much money on it for things like Tyres, Brakes, Exhaust etc etc. (i.e. the wearable items of a typical car) and I think it has a 2 year warranty so I should be only spending on a Service once a year and shoving Petrol in it - I don’t even need an MOT for a few years which is sweet. I wrote the text below in the SOD Blog for 2017 - it pretty much still applies: “Note also that my Subscriptions to Investors Chronicle and SharePad come out of this ‘Spending’ figure - and these probably amount to £450-£500 ish, but I see these as essential Living Expenses !! I don’t have expensive Holidays (this is really down to the physical limitations of being Paraplegic - in all honesty going away just means hassle and health problems for me) and I don’t smoke or anything like that but I suspect if I really tried I could get my Living Expenses down to around £8000 or a bit less (plus Rent on top obviously). Fortunately I don’t need to obsess about getting my Expenses down but of course there is no point in wasting Money and what I don’t spend can be Invested which just makes my Life easier in the future. I keep thinking I spend far too much on Sky TV and BT Broadband etc. - this is an area where I do need to focus my attention.” Conclusion Well without doubt this was a very poor Year for me and not something I wish to repeat too often although of course 2019 has the potential to be very messy. There is obviously a huge temptation to change how I go about things but I am resisting the urge to do radical changes and I think that is the right thing to do. Over many Years I have done very well so it would be silly to abandon an Approach that generally works quite well simply because of one difficult Year - especially because much of it was related to the one-off pain of the Brexit Farce. Anyway, I wrote a lot more specifically on this subject in a recent ‘Weekend Markets Blog’ and you can read that one here and it should give you a good view of my current thinking: http://wheeliedealer2.weebly.com/weekend-markets-blog/a-welcome-change-hopefully That’s all folks, so I will just wish you all the best for 2019 and don’t do anything too silly !! Cheers, WD. Related Blogs First off here is a Blog which I included in a ‘Weekend Markets Blog’ very recently - but it is relevant so I am chucking it in here again in case you have not seen it: http://wheeliedealer.weebly.com/educational-blogs/compare-at-your-peril This one is about how I calculate the Daily Numbers I put out on Twitter every Night and it also should shed light on the contents of this ‘Scores on the Doors’ Blog (there is also a lot of info on the superb and FREE ADVFN App that I use on my Fone and Tablet): http://wheeliedealer.weebly.com/educational-blogs/reporting-end-of-day-numbers-and-the-advfn-app I am throwing the ‘Parameters and Rules Template’ one in here because it is that time of year when we need to be setting our Rules for 2019: http://wheeliedealer.weebly.com/blog/yearly-trading-rules-parameters-template And of course the ‘Power of Compounding’ blog is always relevant here (check out the 20% ‘Magic Number‘ table): http://wheeliedealer.weebly.com/blog/why-bother-investing-the-power-of-compounding As I mentioned in the ‘Spreadbet Account’ Section above, here is the Blog I wrote back in May 2017 about how Costs can eat away at Returns in a Spreadbet Account: http://wheeliedealer.weebly.com/blog/spreads-on-spreadbets-the-hidden-cash-muncher Here is the Final Part of the Blog Series I wrote recently on Income Portfolios - which I reckon is pretty comprehensive and tells all about how I set mine up etc. There are Links at the start to the earlier bits of the Series: http://wheeliedealer.weebly.com/blog/the-joy-of-income-portfolios-part-7-of-7 Here are the Blogs on Spreadbetting that I wrote ages ago now - this is the Final Part but if you go into it there are Links at the bottom to all the other Parts: http://wheeliedealer.weebly.com/blog/how-to-use-leverage-safely-and-successfully-spreadbetting-and-cfds-part-7-of-7 Here are the ‘Stock Buy Checklists’ I produced - this is the Final one with Links to the others at the bottom of it: http://wheeliedealer.weebly.com/educational-blogs/normal-portfolio-buy-checklist-quality-at-a-fair-price-buffett-stock

3 Comments

Jean black

10/1/2019 12:09:52 pm

Very interesting as usual

catflap

10/1/2019 05:54:46 pm

Thanks for posting all the forensic detail, perhaps too much detail. 2018 turned out to be a bit of a headache for everyone.

Ishback

10/1/2019 07:09:43 pm

Thank you for your blog, it's such a great resource. 2018 was indeed a rough year. Lessons I learnt included the importance of proper risk management [guilty on that one], and also the management of emotion / psyche when it all starts to go tits up. I wasn't a full time investor in 2008 or even 2011, and hope that last year will help moving forwards. Leave a Reply. |

'Educational' WheelieBlogsWelcome to my Educational Blog Page - I have another 'Stocks & Markets' Blog Page which you can access via a Button on the top of the Homepage. Archives

January 2021

Categories

All

Please see the Full Range of Book Ideas in Wheelie's Bookshop.

|