|

educational blogs |

|

THIS IS NOT A TIP. I AM NOT A TIPSTER. PLEASE DO YOUR OWN RESEARCH. PLEASE READ THE DISCLAIMER ON THE HOME PAGE OF MY WEBSITES.

Back on Thursday 16th April 2015 I added to my existing position in Empresaria EMR at 64p. This is a business which has struggled for many years with some major problems in Germany and a big Debt Pile. However, it seems like they are back on top form and the Stock looks extremely undervalued - as Readers will hopefully glean from this dive into the guts (that is a horrible expression, Wheelie !!). I have held a very small position in EMR for bloody years. I have had them since about July 2010 - but I always felt that there was something very good here and always planned to buy more once it was clear things were on the mend. Just a shame it has taken so long but the position was only about 0.5% of my Portfolio so it has had little real drag.

I first bought into EMR after hearing Mark Slater go on about them at a Master Investor speech many years back. I was impressed by the Growth Story in Emerging Markets etc. and it looked a great buy. However, it all went badly wrong around July 2011 when they fell foul of a Legal Change in Germany. I can’t remember the details (and it’s pretty irrelevant really) but this hit EMR’s profitability really bad and was a drag on their Results for many years. It also meant that a Debt Pile that had built up when things were going well, was unable to be paid down and became a real burden. This explains why the Shares have been so cheap on a p/e basis for many years - potential Investors were put off by the Debt.

But recently that has started to change. The Company really seems to have got back into its stride and the German Problems are all behind it. The Debt is tumbling fast and the Original Strategy of expanding in Growth Markets around the World is clearly back on song. The beauty is that this has created the opportunity - Investors have still not woken up to the improvement and as you will see from the ‘Valuation’ section below, they look extremely undervalued. Company Overview EMR is a Specialist Staffing business, which has Multi-Brands spread across various Global Locations. They have a deliberate Strategy of diversifying to achieve ’balance’ across Regions and they are targeting High Growth Markets. They have grown over the Years by acquisition but these tend to be small ‘Bolt-ons’ where they use a ‘Management Equity’ model where Entrepreneurial Owners are able to take advantage of being part of a Larger Group whilst still retaining lots of autonomy and a Stake in their Business. I understand from an experienced Recruitment Industry mate that operating in Local Markets across the Globe is very hard to achieve successfully and that many Staffing Groups claim they can do it but in reality it is not true. She confirms that having Local Operations for Local Markets is the way to do it. I guess the Cultural differences and Local Expertise are key here. EMR’s Management Equity Model is explained in detail here: http://www.empresaria.com/investors/equity-philosophy-explained They are biased towards Temporary Recruitment but in Emerging Markets tend to be only involved in Permanent Recruitment. This is because EM’s lack the Legal Structures that make Temporary Recruitment so vital in Developed Economies - I guess Workers are so cheap that you just take them Full Time on no pay !! The NOMAD is Shore Capital. Website The Company’s Website is available here - I was very impressed when looking at this - mind you, it might be because the TSTL one I looked at for a recent Blog was so sub-standard !! http://www.empresaria.com/ Countries of Operation The Countries in which EMR operates are as follows: United Kingdom (bet that surprised you), Germany, Austria, Finland, Estonia, Australia, Japan, India, Indonesia, Thailand, Philippines, Malaysia, Singapore, Hong Kong, China, Chile, Mexico, United Arab Emirates. As I am typing this, it has hit me just what an impressive list that is for a £28m Market Cap company !! Brands EMR uses lots of Brands for different Geographies and Industry Sectors. The full list of Brands can be found here: http://www.empresaria.com/our-brands Industry Sectors

History Here are the key milestones so far:

Strategy I liked this bit so copied it from the Website: The Group's strategy to deliver to the Vision is focused on the following areas:

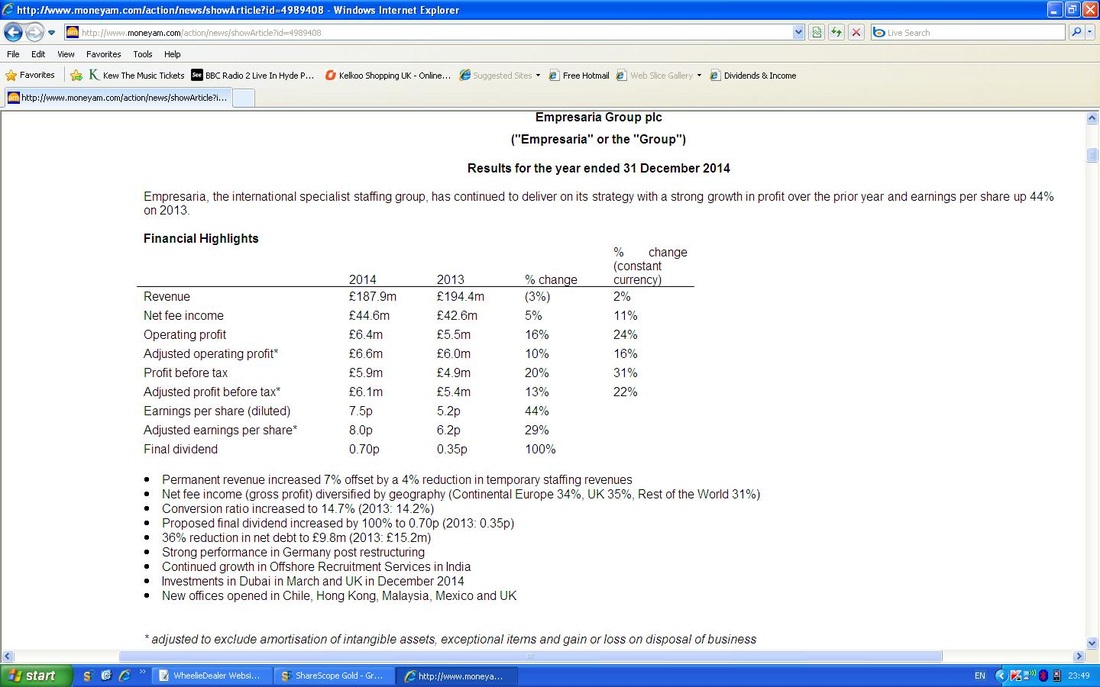

Latest Results Update On the 5th March 2015, EMR issued Final Results for the Year Ended 31st December 2014, you can read the full thing here: http://www.empresaria.com/news/results-for-the-year-ended-31-december-2014 The Headline Numbers are here:

CEO, Joost Kreulen said:

"2014 has been a strong year for the Group with robust profit growth and a number of strategic milestones achieved. Following our brand led strategy, we have continued to invest in our existing businesses, opening several new offices worldwide, and have seen particularly positive results in Germany, India, Japan, Thailand and Australia. The two investments made in the year, BW&P in Dubai and Ball and Hoolahan in the UK, were in line with our continuing strategy of maintaining a diversified balance of brands by geography and sector with Ball and Hoolahan strengthening our existing presence in the Creative and Digital arena and BW&P providing entry into a new geography. We expect both investments to contribute profitable growth for the Group in 2015. We believe that market conditions are favourable and we look forward to growing our business further and creating value for our shareholders." That all reads pretty nicely and the last Sentence is the most exciting bit for me. The Chairman made the following comments: “The Group has delivered a strong growth in profit and earnings per share, and has continued to deliver against the clear growth strategy. The Board is focused on driving further growth to build the business and enhance shareholder value. We see exciting opportunities for growth across our network, particularly from the investments made in 2014, and look forward to the year ahead with confidence.” Anyway, that is all very nice but the bit that really matters here is the Debt situation. Back in December 2013 the Debt Pile was £15.2m (I have taken these figures from the ShareScope Details screen - you can see them below in the ‘Valuation’ section), and it fell to £9.8m at December 2014 - this is a 36% reduction. With £7.05m of Pretax Profit forecast for this Year (2015), the Debt of £9.8m does not seem too bad now - normally I prefer Companies to have almost no debt but I will accept up to 3 times Pretax Profit if the business is predictable and reliable enough. For a Cyclical Recruitment Business, I would think this Debt level is about right - I wouldn’t want it much higher. One thing that does look a bit weak is the drop in Revenues. The Company explained the drop as follows: “In 2014, the Group generated revenue of £187.9m (2013: £194.4m). However, net fee income grew 5% to £44.6m (2013: £42.6m). There were three primary factors that influenced the small decline in revenue during the year: Firstly were adverse currency movements, in particular from Indonesia, Japan and the Euro-zone. On a constant currency basis revenue was up 2% and net fee income increased 11% on prior year. The second impact was lower volumes within the Technical & Industrial sector, due to the completion of a large airport project in the UK and a reduction in lower pay work in line with our strategy of focusing on professional and specialist job levels. Finally, the impact of the prior year disposal and branch closures outweighed revenues generated from the businesses acquired during the year.” On face value, these explanations look plausible - but it is certainly something to watch in coming years - I would expect the Revenues to rise with further Group Expansion and Cyclical Recovery in most Markets. You will note further down that I have made some comments about the Revenue Forecasts for the next few years. Upcoming Dates

Directors If you click this link, you can see the people who run the business: http://www.empresaria.com/governance/directors Director Shareholdings This is copied from the Website:

It is notable that only the Chairman has a really big stake - and his is huge (bet he says that to all the girls). I noticed that on 19th March 2015, Shares Options for the FD and CEO vested and they now have the following additional Shares:

I guess it is a fair conclusion to make that the Directors do have some ‘Skin in the game’ - particularly the Chairman. Major Shareholdings

I note that if you add these all up with the Director’s Shareholdings as well, then the remaining Shares are 37% - so the ‘Free Float’ is probably pretty small. This might explain why it is hard to buy large amounts of the Stock and it is clearly pretty illiquid - which also means it doesn’t take much Buying Interest to get the Share Price moving up fast (or down fast if things go wrong !!) I also note that Mark Slater’s Fund is not in that list - so he must have sold out when they had problems. It will be interesting to see if he buys back in at some point. In recent days, Caledonia Investments have sold down from a 9% Stake to less than 3%. It is unclear to me why they have done this - however, the Shares seem to have been mopped up by Buyers with little problem. Risks

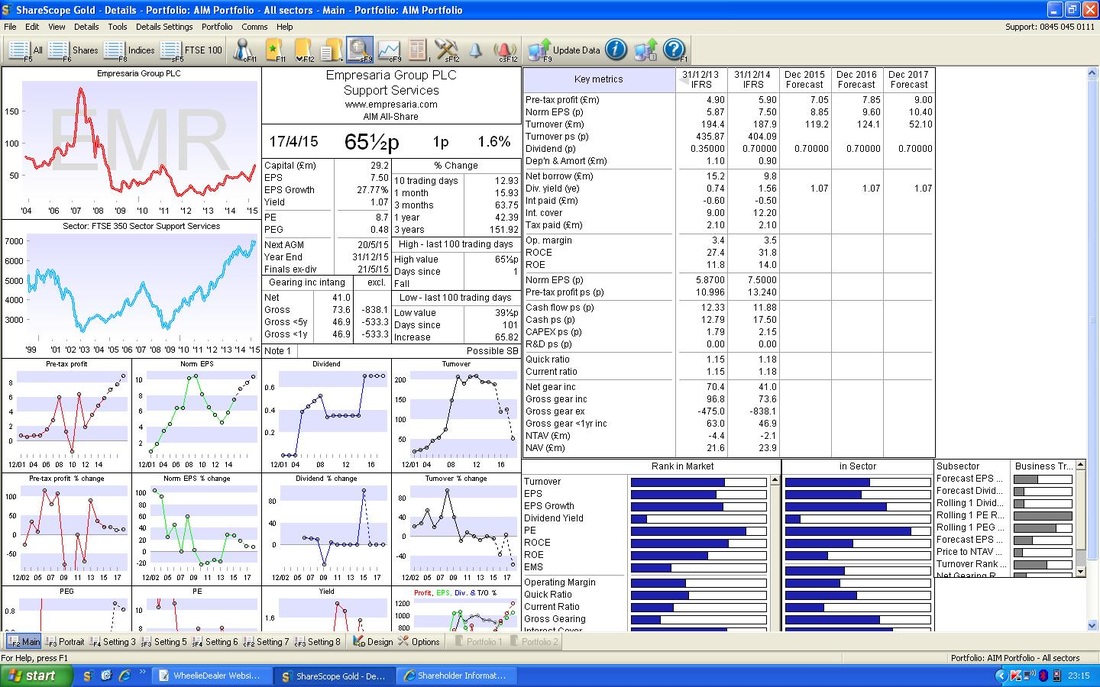

Valuation Here is the ShareScope ’Details’ ScreenShot:

First thing that I don’t understand (does anyone have an explanation?) is that the Forecast Revenue Figures for Dec 2015 onwards are very low compared to the Historic Figures. I have no idea why this is. I would expect the Revenues to rise with Cyclical Recovery and more Offices opening around the World. I know EMR has done a couple of Disposals recently, but I did not think they would have this kind of Revenue Impact.

Another thing that stands out to me here is that targets for EPS look pretty light really - it wouldn’t take many Acquisitions or much improvement in Margins etc. to beat those numbers - maybe we can see Upgrades from Brokers. The Dividends are shown as 0.7p for each of the next 3 Financial Years - that looks light also - maybe we will get small increases. Of course this only applies if the Revenues can rise - I am assuming that the Revenue figures forecasted here are just WRONG. Anyway, based on my Buy Price of 64p, the Price/Earnings (P/E) ratio for this Year 2015 is 7.2 (64p divided by 8.85p) and for Next Year 2016 the Forward P/E is 6.6 - that is daft Cheap (remember, a P/E of 10 is usually seen as good value, and a lower number is theoretically cheaper). With a Payout of 0.7p, the Dividend Yield on my Buy Price of 64p is 1% - this is nothing special. Target Aha, my favourite part of any Blog !! How much am I likely to make on this if it all works out nicely? I think it is very reasonable to put EMR on a Forward P/E Ratio of 12 for Next Year. This would mean a Target of 115p (12 x 9.60p). On my Buy Price of 64p, this would be 79.6% Upside - sweet. That is a lovely and realistic Target to shoot for, but let’s have some fun and stretch things a bit - but still keep it sensible. It would be reasonable to put EMR on a P/E of 15 if things go well in coming months. On this basis, you could easily see a Target Price of 144p (9.6p x 15). This would be 125% Upside on my 64p Buy Price. If we go really mad, we could up the EPS for 2016 a bit to 10p and put this on a P/E of 18 - that would give a Target Price of 180p. This might seem pretty fanciful, but I think it is very possible in reality. As ever, the key is PATIENCE. Technicals Normally I show the Charts that prevailed at the time I bought my Stock, but as that was a few days ago, I will show the situation as it is today, Monday 20th April 2015. If you look at the Chart below, this is a Long Term view, going back about 6 years or so. As a thing to note, Long Term Charts and Features from the Long Term in Technical Analysis, always dominate over Shorter Term Charts and Features - worth remembering this and I always start looking at any Stock on the longer view first. The thing to note here is that the Stock is in a pretty nice Uptrend Channel from around 2012 - I have marked this with the Black Line at the bottom and the Red Line above. The Black Arrow points to where the Price finished today - as you can see, it is at the top of the Uptrend Channel and this may mean that in the Short Term it will fall back a bit before the Uptrend can continue. The other important feature here is marked with the Blue Arrow. This is a Horizontal Resistance Line at about 70p - it may be hard to get through, but a Breakout here would be a Very Strong Buying Signal. The Chart also suggests that if it can Breakout, then just under 80p and 90p may cause trouble but it should get to 100p quite fast.

In the Top Window of the Chart below, you should be able to see the Uptrend on a much shorter timescale - this is going back a couple of years. Hopefully you can see that the Price is very near the Top of the Uptrend Channel.

In the Bottom Window, I have marked with a Blue Arrow that the RSI (Relative Strength Index) is very high and I would expect it to fall back from here - obviously not what I want to see as I have recently bought the Stock, but I am a Long Term Investor and such gyrations don’t overly bother me. With a Stock this undervalued, I would rather be in the Game than trying to time my Entry to perfection and missing out. I see this a lot where people try to get a Perfect Entry and the Stock runs away from them and they miss a big gain. I tend to buy a small Position first if I think it is a bit Toppy in the Short Term - it is drops, I can buy more. For me it is often the case that I really want the Stock because the Fundamentals stack up nicely, the Technicals are secondary.

The Chart below shows the Bollinger Bands in the Upper Window. I have marked with the Black Arrow that the Price is currently up above the Top Bollinger Band - this is an unusual situation and I normally find that the Price will fall back into the Bands in coming days.

In the Lower Window, I have marked with Blue Arrows where a MACD Crossover (Moving Average Convergence Divergence) took place - this is a bullish sign and I bought pretty much just after this Crossover. The Lines and the Histograms are just different representations of the same thing - MACD.

The Chart below is much Shorter Term with just a few Months. The Red Arrow points out that the Strong Moves up of recent days (with the Big White Up Daily Candles) have eased now - this might mean the Price will fall back a bit or it might consolidate and go sideways for a bit, before a move higher.

The Green Arrow points out where the 50 Day Moving Average and the 200 Day Moving Average have done a Golden Cross - this is usually a good sign that the Stock is likely to rise in coming Months.

I think the over-riding impression I get from these Charts is that the Price may ease back a bit in the coming weeks, but then will continue heading up. Of course there are no guarantees but it seems most likely. I will not be complaining if it just keeps charging upwards !!

Conclusion I have had to be very patient with this Stock but it is finally starting to payoff and I am nicely in Profit on my Initial Purchase from years back. I think the appointment of Joost as CEO in 2012 was a bit of a turning point and the Company looks to be back on song after its issues in Germany. Obviously there are Risks, but on a Current P/E of 7.2 those Risks look well Discounted and I think the Upside here is lovely. Risk / Reward looks very attractive to me. The revenue forecasts on ShareScope make no sense to me - I am happy to overlook this Negative as it just looks totally wrong. If anyone can enlighten, please comment below. It would be great to see the Debt come down more but I would be happy if the Debt stays around the same level as now but they continue with careful Acquisitions and grow the Group - the future does look pretty sweet. noson dda, wd

1 Comment

Wheelie

20/4/2015 02:37:05 pm

@imranyawan on Twitter has let me know that the Revenue Forecasts on Stockpedia are £193m for 2015 and £202.3m for 2016 - these look more sensible than the ShareScope figures which are clearly not right. Cheers, WD Leave a Reply. |

'Educational' WheelieBlogsWelcome to my Educational Blog Page - I have another 'Stocks & Markets' Blog Page which you can access via a Button on the top of the Homepage. Archives

January 2021

Categories

All

Please see the Full Range of Book Ideas in Wheelie's Bookshop.

|