|

educational blogs |

|

THIS IS NOT A TIP OR RECOMMENDATION. I AM NOT A TIPSTER. PLEASE DO YOUR OWN RESEARCH. PLEASE READ THE DISCLAIMER ON THE HOME PAGE OF MY WEBSITE. IF YOU COPY MY TRADES, YOU WILL PROBABLY LOSE MONEY.

Devro DVO is a stock I have invested in before and I note that it has put out some weak results over the last year or so and has got quite beaten up - it is at 3 year Lows so maybe there is Value here and I quite like the idea of having something that is food related (they do Skins for Sausages) in my Portfolio as I don’t really have any exposure here. From a quick glance the usual Investment Ratios like Forward P/E and Divvy Yield etc. look ok, but the big stand out is the Debt - this has shot up in the last year and obviously creates some sort of Risk if it is not manageable. From what I understand, much of the problems (and the High Debt) stem from delays in getting a new Chinese Factory up and running - my hunch is that maybe once the Factory is on stream, Costs will drop and we will see Debt start to fall quickly - if so, then the extra Capacity could give DVO a lot of new Growth Potential and I suspect the Market is totally missing this important point.

I wanted to write this Blog as a discipline to make me do a deep dive analysis and see if my hunches about Growth are correct. If everything stacks up, then it could be an opportunity to buy in at a Low Price to a Growth Stock with a proven Track Record and potentially a lot of upside (we like that !!).

After writing the above Paragraph, I decided on Wednesday evening that I was happy with various aspects covered in the Blog and on Thursday 29th September 2016 I bought a small Share Position at 241p. I expect to add to this as opportunities arise. Company Overview I have copied the text below from the website because it looks simple enough to understand and saves me thinking !! “Devro is one of the world’s leading suppliers of collagen casings for food, used by customers in the production of a wide variety of sausages and other meat products. Collagen is a naturally occurring polymer which is transformed into gel, tubular casing and film at Devro’s manufacturing sites in the USA, UK, Czech Republic and Australia. Devro employs over 2,200 people, with skills and knowledge ranging from chemical and electrical engineering to food technology, meat science and environmental health. Over 100 staff are in daily contact with more than 1,000 customers, providing specialist technical advice and support for sophisticated food manufacturing operations in more than 100 countries. Regional Business Directors have responsibility for day-to-day sales and manufacturing operations, with profit accountability. Strategy, financial policy, marketing and information systems are managed centrally, with an Executive Management Committee and a Board of Directors providing leadership and experience.“ They also have Sales Offices in Moscow, Auckland, Beijing, Hong Kong, Tokyo & Miami. There also seems to be a Manufacturing Plant in the Netherlands which isn’t mentioned in the text above and of course they should soon have the new one in China. The Company lists the following ‘Growth Drivers’:

To flesh that out a bit, the trend that helps DVO is that as people in developing Economies move from Rural areas into Cities, they tend to earn more and go for a higher protein diet - in other words they eat more meat. In many of these Countries it is seen as a sign of affluence and aspiration to eat meat. Company Website www.devro.com Key Risks

Products There is clearly a lot more to ‘Sausage Skins’ than perhaps you may at first think - from what I can tell, there seem to be 4 basic Product types DVO provide:

WD Interlude. Hey, I was watching Discovery Channel the other night and they had this thing about Parachutes and how they are designed and stuff. Anyway, the interesting bit was they have already got small Planes with built in Parachutes that lower the WHOLE PLANE down when you deploy them - already saved a few lives. Some geezer was saying he thinks they could do it for Commercial Jetliners at some point but the issues are around size, weight and strength. You can get more excited about Sausage Skins here: http://www.devro.com/our-products/overview/ Strategy DVO claims they have 3 Strategic Priorities:

I think DVO gets a degree of Competitive Advantage (Moat if you like) from its established relationships with Customers and its Research & Development capability and technical expertise. The following Text is taken from a Presentation I found on the Website and refers to Strategic Investments:

Competitors I have struggled with this section - I was expecting there to be several major Manufacturers and Suppliers of Sausage Skins who compete with DVO but I have struggled to find much of use. From a search on Google I have come to the conclusion that there are many Suppliers but they seem small and I don’t recognise any names. If this is correct (it could well be wrong, I might be missing something really obvious), then it suggests to me that DVO is one of the larger producers in a pretty niche market - this could be a good thing. It also suggests that there is scope for Consolidation by DVO to buy up some of the smaller players as ‘Bolt-on’ Acquisitions. Obviously this is something for the distant future though as with the current Factory ramp-up they do not have the Balance Sheet firepower to safely do anything more than perhaps the odd tiny Acquisition. After writing the above text, I heard from top Geezer Jonathan Curry (@jpsc01 on the Tweetster) that DVOs main Competitors were Viskase and Visconfan (and one other Japanese company that he couldn’t remember the name of). It is clearly a Competitive Market and Investors need to be comfortable with DVOs position within it. You can find more detail on these Competitors below. Viskase Viskase appears to be US based and has operations in North America, South America, Europe and Asia - in fact, the footprint looks very similar to DVO. It looks to be a bit bigger than DVO but not much. You can find out more about Viskase here: http://viskase.com/ Viscofan This is a Spanish company and again has a similar footprint of geographic locations to both DVO and Viskase. It looks to me like Viscofan is the largest of the 3 but not by all that much. You can find out more here: http://www.viscofan.com/EN/Pages/default.aspx Risks:

Listing Details

Note: I like the fact it is Fully Listed - this is mainly because AIM Companies are often outside the Mandate of many Fund Managers so they are not allowed to buy them. Being Fully Listed means there are more likely to be plenty of Buyers (and liquidity) for the Stock - obviously as Share Buyers we need other people to come in and buy the Stock at higher Prices than where we entered. Decent Liquidity also means we can sell Shares in future when we want to without finding we are unable to shift a large Position. Resistered Office Moodiesburn, Chryston, Scotland, G69 0JE. Auditors KPMG LLP 15 Canada Square London E14 5GL. Covering Brokers

That’s an interesting list - shows the Company gets a lot of Broker Coverage which can be very useful when things are going well !! “Brokers - in a Bull Market you don’t need them, in a Bear Market, you don’t want them !!” Annual Reports The Latest Annual Report for 2015 can be found here: http://www.devro.com/investors/annualreport2015/ Older Annual Reports can be found here as PDFs: http://www.devro.com/investors/annualreport2015/previous-annual-reports/ Company Presentations There are loads of Presentations that have been given to Analysts by the Company available as PDFs here: http://www.devro.com/investors/broker-coverage/analyst-presentations/ Financial Calendar

Company History This is from the website, there is not a huge amount of info about this:

Directors The Key Directors are (I have copied much of this from the website):

You can find a fairly large list of the Directors here with brief summaries: http://www.devro.com/about-us/who-we-are/ Director Shareholdings There is loads of information around Director Shareholdings, Remuneration and Incentive Plans in part of the Annual Report 2015 which you can view here: http://www.devro.com/fileadmin/files/devro-ar2015-2.4-directors-remuneration-report.pdf As a speedy summary, the Shareholdings at the 31st December 2015 were:

Since the date of those Shareholdings, the following Transactions by Directors have taken place:

Major Shareholders This text is taken from the Annual Report 2015: “As at 31 December 2015, the company had been notified of the following material interests in the issued ordinary share capital of the company:

During the period 1 January 2016 to 4 March 2016 the company received no additional notifications of material interests in the issued ordinary share capital of the company under DTR5, other than a notification from Templeton Investment Counsel LLC that it holds less than 5% of the company’s issued ordinary share capital, having previously advised the company during the same period of a holding above the 5% threshold.” On 21st September 2016 Neptune Investment Management Limited went Above 13% & 14% - so these guys are really increasing their Stake. There were other Transactions by them prior to this. A very good sign I think. Please note, for time reasons I have not looked laboriously through all of the RNS releases over 2016 to analyse movements in Shareholdings. For my purposes, the information above is enough to make me reasonably happy that DVO has Institutional Support - the Neptune Holding is of particular interest and gives me confidence in the likely future for DVO. Recent Trading DVO issued an Interim Report on 3rd August 2016, you can read it here: http://www.devro.com/uploads/tx_sbdownloader/Interim_Results_Announcement_HY_2016.pdf This is the critical part and the increased ‘Exceptional Costs‘ and delays caused the Shares to sell off heavily: “Transformation of manufacturing footprint now in final phase

However, note the following from the CEO’s comments: “The Board’s expectations for the full year underlying operating profit remain unchanged. The transformation programme has reached its final phase. The next stage of strategic development will focus on growing sales through improved commercial capabilities, introducing the next generation of differentiated products and further improving manufacturing efficiencies.” My take from this is that they have had some issues with the new Factories and this has slowed things up and added to Costs (the original forecast of Exceptional Costs was £14m rather than the new figure of £20m) - however, they still expect to meet Full Year Guidance and the focus will now move to taking advantage of the extra Capacity that the new Factories and Products provide. I am always keen to see Companies expanding their Capacity to supply Products - decisions about new Factories (and Warehouses, Outlets, Delivery capabilities etc. for many Businesses) are not taken lightly and show a high degree of confidence by the Directors that they see Growth Opportunities ahead. Quite often a Company can manage increases in Demand by just expanding existing Facilities - taking the step of building new Factories (in DVO’s case, 2 of them) is not a snap decision. It also shows that they expect the increased Demand to endure - if it was just a temporary spike up, they would meet it simply by sweating existing Assets. This bit about Sales is important: “Revenue for the first half was unchanged year on year, having benefited from exchange rates which offset a 7% reduction in sales volumes. Of this reduction in sales volumes 40% related to China, but this had little impact on profit given the low margins earned on products that have historically been imported. In addition approximately 40% of the reduction related to the Europe segment, in particular Russia which continues to experience difficult economic conditions. Of the remaining reduction approximately half related to Latin America, which is the region most significantly impacted by our manufacturing transformation programme.” The problems in China are partly because there is an Oversupply of Cheaper Sausage Skins and DVO is moving upmarket with a more Premium offering. This bit explains more about Russia - this looks to me to be a big problem for DVO and it will be interesting to see how this evolves - it is clearly a Risk: “The economic environment in Russia continued in line with that experienced in the second half of 2015. Devaluation of the local currency has increased the cost of importing and Devro has responded by developing a specific product offering for this market. Overall revenue was down 19% (down 26% in local currency).” This bit fleshes out the Latin America situation - it looks to me like most of the problems here were caused by disruption from the Factory changes: “Latin America is the region most affected by the transformation programme, in terms of the scale and complexity of the transfer of customers onto new products and also temporary capacity constraints during the transition. Revenue was down 9% in the first half (down 15% in local currency).” They also seem to have problems in part of Asia: “Sales performance in South East Asia was mixed with good growth in Korea and Indonesia, but weaker trading in Thailand. Revenue was down 6% (down 13% in local currency). In Australia & New Zealand overall demand was lower in a market where Devro has a major market share. Revenue for the first half was down 5% (down 7% in local currency).” There was a bit of more positive news - in both Europe and North America Sales were up 8%, which seems pretty decent as these are more mature markets - and don’t forget DVO Management have said they expect to meet Full Year Guidance despite their issues. DVO give more details on the new Factories here: “Transformation plan update Now that commercial production has commenced at both of the new plants in China and the US, the manufacturing transformation programme has reached its final stage. The China plant commenced production in the first half ahead of plan, and has already achieved the initial planned level of manufacturing efficiencies. Commercialisation of products with customers has commenced, focused on the target customer base in the premium segment. This process is expected to continue until the end of 2017 and, as a result, the new China plant is now expected to contribute to profits from the beginning of 2018. In the US the old factory is now closed, a major milestone in this investment project. Production commenced at the new plant in the first half and we are now in the process of transferring almost all customers in the Americas to products from different manufacturing locations as part of this transformation of our manufacturing footprint. This involves working closely with customers through their requalification process, refining the products to meet customers’ needs and scaling up production of the final products. Due to the complexity of the transformation the transition period for the new plant will be longer than originally planned, although is still expected to be completed by the end of 2016.“ This bit on FOREX is worth noting - especially the boost in H2 if low Sterling persists: “Foreign currency Devro operates worldwide and with multiple currencies. Major transactional exposures arise from sales in euros, US dollars and Japanese yen whereas manufacturing costs are in Australian dollars, Czech koruna, US dollars and sterling. Devro operates a hedging programme to manage the volatility associated with transactional exposures. Translational exposures arise from the conversion of the results of all our businesses into sterling. In the first half of 2016 there was a general weakening of sterling, with a significant further movement in the last month following the EU Referendum vote on 23 June 2016. These movements contributed £1.4m of translational exchange benefit to underlying operating profit for the first half, and if current rates remain in place for the remainder of the year we would expect further benefit in the second half.” Debt Without doubt many Investors will be put off by the increase in Debt but in many ways this is creating the opportunity to buy into a High Quality Business at a fair Price that is going through some Short Term Issues as it expands. I see no problem here, as the text below will attest. This comes from the Interim Results: “Cash flow and net debt Devro continues to be a highly cash generative business. In order to fund the significant investments made as part of the transformation of the manufacturing footprint, additional long term facilities were put in place in 2014 to supplement the shorter term facilities. As the three year investment programme comes to an end, net debt increased to £147 million at 30 June 2016 (or £153 million including derivative liabilities), compared with £126 million at year end 2015. This includes the effect of a significant weakening of sterling in June 2016 (given that a part of the group’s debt is denominated in US dollars) following the result of the EU Referendum vote on 23 June 2016, which increased the reported net debt figure at 30 June 2016 by approximately £15 million (including the effect on derivative liabilities). At 30 June 2016 the net debt to EBITDA ratio was 2.9 times and the EBITDA to net interest payable ratio was 9 times, meaning both ratios were within their limits (of <3.25 times and >4 times respectively) despite the recent changes in exchange rates. There will still be some cash outflow in the second half related to the transformation, both in terms of capital expenditure and exceptional items, but by the end of the year the Board expects the net debt to EBITDA covenant ratio to be lower than at 30 June 2016. Following completion of the transformation, cash generated from the business will enable net debt levels to be reduced, resulting in the covenant ratios returning nearer to historic levels.” Two bits stand out to me there - the first sentence about Cash Generation and the last Paragraph about how they expect Debt Levels to be reduced once the new Factories are fully on line. Cash Flow Looking at the Cash Flow Statement, the following Numbers matter (all this text is derived or copied from the Interim Results):

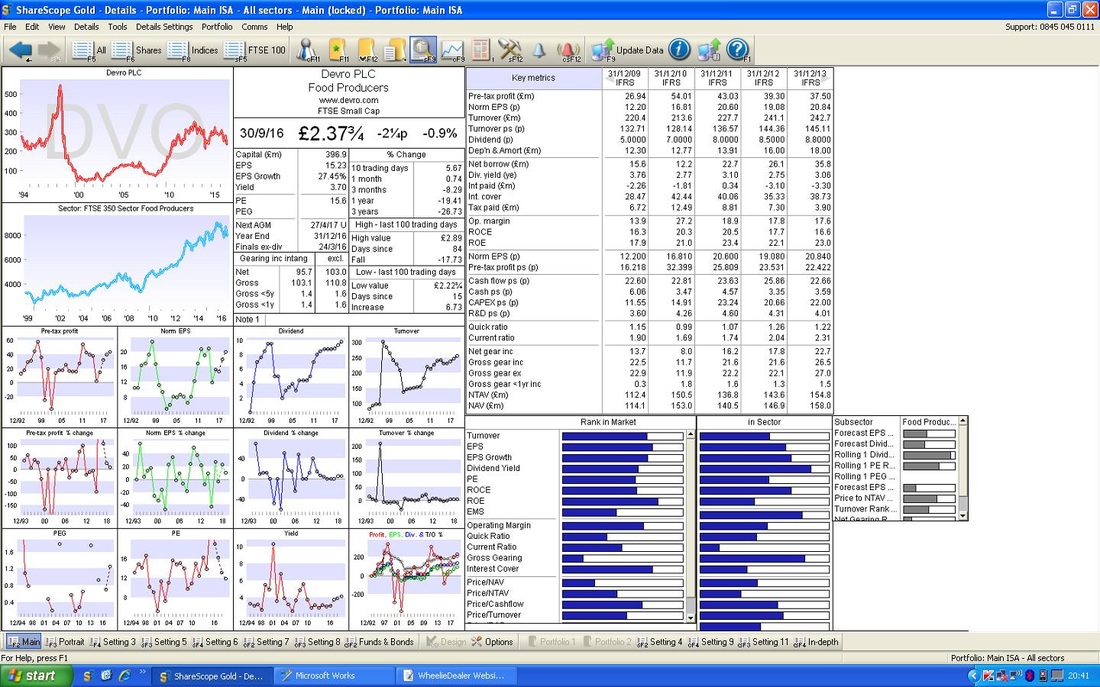

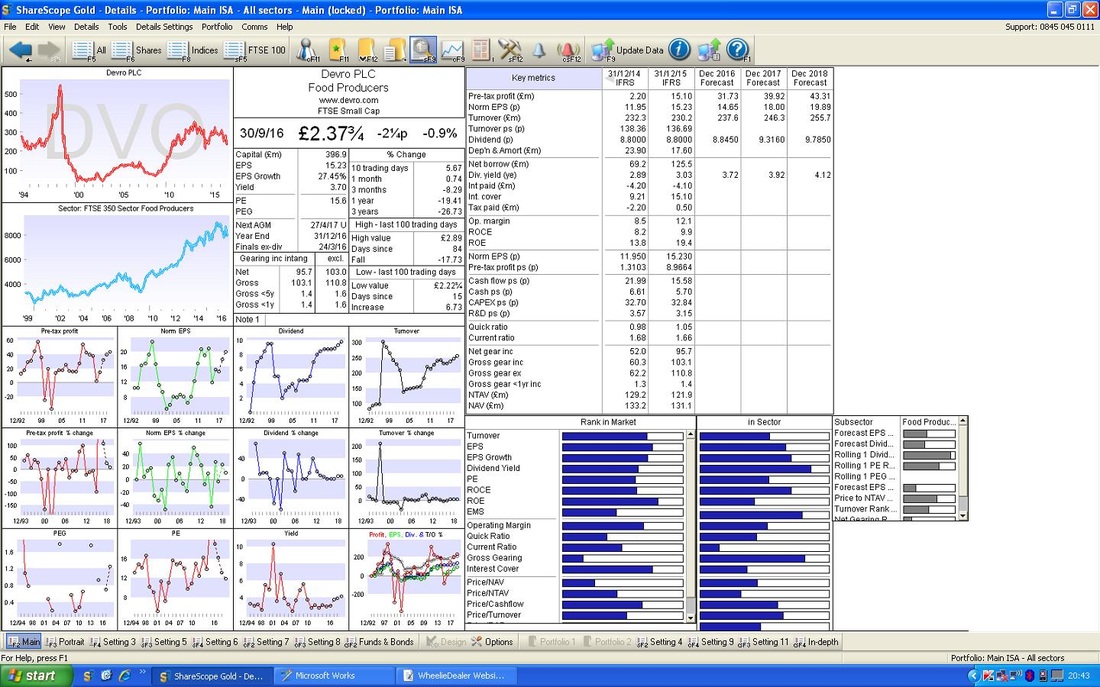

Cash Generated from Operations was £13.8m (before Interest and Tax) and Operating Profit was £18m (again before Interest and Tax) so clearly if the Interest Cost gets reduced and Profitability improves, then the Dividend is not at risk. Note the following regarding the Dividend - this shows the Divvy is safe for a while: “The final dividend of 6.10 pence per share in respect of the year ended 31 December 2015 was paid on 13 May 2016, absorbing £10.2 million of equity. The interim dividend of 2.70 pence per share, which will absorb an estimated £4.5 million of equity, will be paid on 7 October 2016 to shareholders on the register at 26 August 2016. This compares with the 2015 interim dividend of 2.70 pence per share, which absorbed £4.5 million of equity.” Further down in the Interim Report I note the following under Note 16 ‘Cash flows from operating activities‘: “Cash generated from underlying operations - £26.3m Exceptional items cash outflow - (£12.5m) Total £13.8m.” So once the Exceptionals mostly go away as the Factories are sorted, the Cash Generation is in fact very high and more than sufficient to pay the Dividends (and hopefully if the Business gets back on track we will see increasing Dividends). Pension This text appeared in the Interim Report: “Net finance cost on pensions for the period amounted to £1.1 million (2015: £1.1 million).” And further down it says: “The group’s net pension obligations increased to £77.9 million at 30 June 2016, from £56.4 million at 31 December 2015, which primarily reflects a decrease in discount rates across the group schemes.” Clearly DVO is like so many other businesses facing difficulties with Pension obligations - however, it is clear that once the Factories are resolved they have scope to get on top of this problem (if it is one - a change in the Discount Rate or perhaps a Legal Change by Parliament regarding Pension Fund Accounting and the problem could vanish instantly. That is the nature of Pension Fund numbers.) Valuation The Piccie below is a ScreenShot taken from the ShareScope ‘Details’ screen as at Friday 30th September 2016. The first one in the sort of Right Hand Top Quarter of the Screen has Historic Results going from 2009 to 2013 - I have simply put this in for Readers’ interest. The next Screen does 2014 and the Forecasts as they stand now.

If you look in the Top Right Hand Corner on the second ScreenShot, then you should see ‘Norm EPS (p)’ for ‘Dec 2016 Forecast’ of 14.65p (this is a Consensus Figure and I assume it is made up of many forecasts because DVO has a lot of Analyst coverage as we saw earlier). At my Buy Price of 241p on Thursday 29th September 2016, this gives a Forward P/E Ratio of 16.4 (241p divided by 14.65p) which doesn’t sound amazingly cheap. However, it is worth bearing in mind that this will be impacted by the Factory Delays so it is probably not all that representative of what DVO can generate in Earnings in future years.

If you look at the figure for ‘Dec 2017 Forecast’ we get 18.00p of EPS - on my Buy Price of 241p this gives a Forward P/E Ratio of 13.4 which sounds pretty fair for something that is very likely to grow in coming Years and to generate a nice growing Dividend. In addition, I suspect we could see Earnings Upgrades if DVO can exploit the new Capacity and drive efficiency throughout the business as outlined in their Strategic Imperatives. If you look at the ‘Dividend (p)’ line for ‘Dec 2016 Forecast’ it says 8.8450p, on my Buy Price of 241p, this gives a Forward Dividend Yield of 3.7% (8.8450p divided by 241p multiplied by 100%). If we go forward a year, the Dividend Forecast for 2017 is 9.3160p which on my Buy Price of 241p gives a Forward Dividend Yield (2 years out) of 3.9% - which isn’t too shabby for a Defensive Stock in this World of crazy low Interest Rates and low Returns on almost everything. Targets Obviously the key to making Capital Upside on DVO is how well it gets a grip on the Factory delays and exploits the extra Capacity that will consequently be at their disposal. At the moment Sentiment is very poor and the Stock is not loved much, and of course this is where any opportunity comes from. Once Sentiment picks up as DVO (hopefully) announce good progress in future Trading Updates, we should see the Shares trade on a higher rating - particularly as the Debt falls. I think it is very possible that DVO could be back on a Forward P/E of 18 and if we work off the Forecast EPS Figures for 2017 of 18p, this would give a Target of 324p (18p multiplied by 18) which would be 34% Upside on my Buy Price of 241p. OK, let’s stretch things a little. Let’s assume DVO does the business and beats Analyst Expectations and comes in with 20p of EPS for 2017. This would give a Target of 360p (20p multiplied by 18) - which would be 49% up on my Buy Price of 241p. Of course this ignores the Dividends I expect to receive and I think DVO is a Stock I can happily hold for many Years to come, and with such a Holding Period, I expect the ultimate Target a few Years down the line could be way higher. It is worth bearing in mind that I will soon be picking up near 4% Dividend and this is very likely to grow year on year so it could become a very nice Income Stock. It is also possible that Earnings could be higher in future years if DVO does some more Bolt-on Acquisitions and of course there is always the possibility that DVO itself might get taken-over. As I have explained, my Initial Purchase is very much to get my ‘Foot in the Door’ and I would love it if I can be buying more at lower Prices - if I can buy more down near 200p I would be really happy. Technical Situation First off let’s do the ‘Big Picture’. The ScreenShot below from ShareScope goes back to about 2007 and really shows how we had an Uptrend (marked by the Black Line with the Black Arrow) which ran for many Years until the Share Price broke below the Black Line where my Yellow Circle is. Note the High up at 381p which was hit in February 2013 - this is not in fact the All Time High - back in 1998 it got up near 550p but it doesn’t really have much Charting validity all these years later I think.

The Screen below shows the DVO Price going back about just over a year. The Black Line is the same one that was on the Chart above, and the Red Line (marked by my Red Arrow) shows a Downtrend Support Line for most of that time. The Green Horizontal Line (marked with the Green Arrow) should give quite Strong Support if the Price falls more in coming Weeks - this is at about 218p. If that level fails, then I would expect the Price to drop down to 200p - that would be a pretty nice Price to be buying at I suspect.

My Blue Horizontal Line (marked with my Blue Arrow) is up at about 241p and is pretty much where I put in my Pilot Purchase - as you can see my timing was abysmal because it looks likely to drop back in the Short Term !! Note both the 50 Day Moving Average and the 200 Day Moving Average (those Blue Wiggly Lines) are falling - first off we need the 50 Day to level out and hopefully in the not too distant future we will get a Bullish ‘Golden Cross’ where the 50 Day MA moves up and crosses the 200 Day MA - this may take a while sadly

Things I like about DVO

Things I’m not so keen on

Conclusion I am really impressed by this Business. I have traded DVO many times in the past so I knew them reasonably well before I started work on this Blog but having now dug very deep I feel quite comfortable with making a small Purchase as a ‘Starter Position‘ to get my foot in the door before buying more over time. When I started looking at DVO it was the Debt that stood out as the big worry and this is probably the main reason why the Shares have got spanked recently - in fact, talking to several Investing mates recently the reaction from pretty much all of them was “strewth Wheelie, that’s got a lot of Debt” - which of course is true. However, having dug into the Cash Flow situation I am comfortable that DVO will come out the other side very well and the increased Capacity will give the ability to ramp up Sales and Profit’s a lot. I think DVO is an excellent Long Term Play. The increase in Holdings by Neptune to 14% is a major Positive and this has probably been the thing that has really switched me to Buy Mode on DVO. It seems very possible to me that DVO might be a Takeover Target, particularly for an overseas based Food Group. In the UK, there are companies like Cranswick CWK and Hilton Food Group HFG that might be potential Suitors. This is mere speculation, but it must be a possibility. Of course there is a flipside to this - it is very possible that I will buy into DVO in the hope of holding it for several Years and making nice, leisurely, gains, only to have it stolen from me by a Takeover Bid (High Class Problem obviously !!) At the moment I have no Food Producers in my Portfolio and it is a bit of an omission. Up until recently I did have Finsbury Food (FIF) but I was never really happy with their pretty aggressive Acquisition Strategy and ultra-competitive environment, so I sold out with a nice Profit - but of course it has left a ‘Food Producer’ shaped hole in my Portfolio. Overall I am pretty nervous about the Macro picture at the moment and I do not want to take big Long bets on anything - so a Starter Position gets me in and I will look to build over time. At the moment I have about 1% by Portfolio Value of DVO Shares and I will take opportunities when they arise to increase that Stake. I expect to get up to around 3% to 4% of my Portfolio Value in coming Months, via a mixture of Shares and Spreabets. I hope Readers found the Blog interesting and useful, Cheers, WD.

6 Comments

Steve Holdsworth

4/10/2016 01:36:24 pm

Hi WD,

WheelieDealer

5/10/2016 09:40:05 pm

Hi Steve, great that you enjoyed the Blog - as you probably remember from my NPT Blog (I think it was that one) I am really trying to be balanced on the Good and the Bad on these Stocks because it helps me clarify my thinking and of course it gives Readers a big help in understanding the factors that can affect such Stocks.

RalphMilsap

4/12/2016 04:40:55 am

I think by now it is clear that Steve knew much better what was going on inside Devro than WheelieDealer. I read what WD wrote and realized the research was pretty much all surface stuff simply pulled off Devro's website.

WheelieDealer

7/12/2016 08:45:27 pm

Hi Ralph Milsap, Thanks for the comments - some useful info there. You're dead right - much of the info in my blog was collating info from the Website and I did not know the in-depth detail that you know about the Senior Managers and the history - and I cannot say I am an expert on the Collagen Casing Market !!

RalphMilsap

8/12/2016 02:53:43 am

WD,

WheelieDealer

9/12/2016 12:23:55 am

Hi RalphMilsap, No worries, what you said is actually very fair comment and clearly you know DVO very well yourself. If you look at my Blog Page on 14th Nov I wrote a follow up blog with my thoughts on where we are now - it might be worth a look. I will be amazed if DVO avoids a Rights Issue but I think a Management Shake-up would help as well. For now I am sitting things out and seeing how it develops but I was pleasantly surprised to see quite a bit of Director Buying in recent days - it looks a bit more than token buying. Leave a Reply. |

'Educational' WheelieBlogsWelcome to my Educational Blog Page - I have another 'Stocks & Markets' Blog Page which you can access via a Button on the top of the Homepage. Archives

January 2021

Categories

All

Please see the Full Range of Book Ideas in Wheelie's Bookshop.

|