|

educational blogs |

|

THIS IS NOT A TIP OR RECOMMENDATION. I AM NOT A TIPSTER. PLEASE DO YOUR OWN RESEARCH. PLEASE READ THE DISCLAIMER ON THE HOME PAGE OF MY WEBSITE. IF YOU COPY MY TRADES, YOU WILL PROBABLY LOSE MONEY. I HAVE A VERY LARGE PORTFOLIO AND I USE DIVERSIFICATION TO SPREAD RISK ALONG WITH TRICKS LIKE HEDGING AND OCCASIONALLY BY THE USE OF STOPLOSSES - IF YOU BUY ANY STOCK YOU REALLY SHOULD FOCUS ON HOW IT FITS IN YOUR PORTFOLIO AND KEEP RISK MANAGEMENT AT THE FOREFRONT OF EVERYTHING YOU DO. BE AWARE THAT ALL INVESTORS/TRADERS GET THINGS WRONG AND MANY STOCK SELECTIONS WILL WORK OUT BADLY - MAKE SURE YOU UNDERSTAND THIS. WATR IS A PARTICULARLY SMALL STOCK AND IT HAS A HUGE BUY/SELL SPREAD AND IS HIGHLY ILLIQUID AND THEREFORE HIGH RISK.

I have been interested in this Stock for a while - I think it first came to my attention when my mate @MGinvestor on twitter bought into it and I seriously rate his abilities to find very good undervalued small Stocks so it got my attention. The thing I particularly like is that I have been aware of all the stories about Environmental stuff and how Water will be the most valuable commodity on Earth soon and how there will be Wars fought over Water and all that Armageddon type nonsense - but however much of such bilge I read, there is clearly a grain of truth here somewhere but I have found it extremely difficult to find a Water Stock to actually enable me to play the Mega-Theme. There are of course the usual Water Utilities but they are of course hemmed in by Regulation and are more like Dividend Income Stocks than the Growth Play I really want.

Population Growth is a major force around the World and most Western Economies have growing Populations from people living longer and immigration from poorer Regions - these and other factors are increasing pressure on Water Supplies and make it inevitable that Governments will become ever more focused on Leakage and the need for speedy detection and repairs. Climate Change could also add pressure to reduce Water Leakage.

Water Intelligence WATR seems to be the beastie I am looking for - so I am producing this Blog partly to give Readers something to read but for a much more selfish reason I have used it to give my Research into WATR some structure and this led me to Buying into the Stock on Wednesday 16th August at 130p (more details are shown on the ‘Trades‘ page). Introduction to WATR You can find the Company Website here: http://www.waterintelligence.co.uk/ I have to say it is a very limited Website and there are several errors on it - like a link to ‘Our Business in Action - Videos’ which contains no videos. From a trawl around the Website I found this page particularly good as an Introduction to both the Water problems facing the World and as a good introduction to WATR’s capabilities: http://www.waterintelligence.co.uk/water-facts/ WATR is the 100% Owner of an American Subsidiary called ‘American Lead Detection’, which it has owned since 2009 when there was a Reverse Takeover by ALD of Qonnectis in the UK. I copied this text from the Website, it explains pretty well what WATR do and where they do it: “Established in 1974, American Leak Detection provides non-invasive water leak detection and remediation services throughout the United States, as well as in Canada, Australia, Spain, Belgium and select other countries. Unlike traditional plumbing methods, American Leak Detection leak specialists locate and pinpoint leaks without the breaking of walls or floors. Its technicians receive training in proprietary methodologies and use innovative technology including infrared, acoustic and correlation equipment. These non-invasive leak detection methods and technology significantly help lower repair costs and conserve water. American Leak Detection’s corporate and franchise units service thousands of homeowners and commercial businesses each year. Leak survey and detection work is also provided to municipalities and water systems as these utilities seek to reduce non-revenue water usage and water loss.” In the UK, American Leak Detection provides similar services via the name ‘TargetLeak Detection’. Qonnectis I copied this bit from the Website: “The Group’s product business is operated through Qonnectis Networks Limited, which provides a managed service to water and energy utilities that allow for remote and automated meter reading, data storage, analysis and presentations of meter data via the Internet. Information from meters is logged remotely, stored and then sent to the Qonnectis data centre. It can then be accessed by customers for billings and for subsequent analysis. Customers can receive e-mails or SMS text messages in the event of surges in the use of electricity, gas or water. This can help pinpoint unusual consumption patterns of gas or water leaks. Qonnectis’ customers include Thames Water, NHS Hospitals, the London Fire Brigade, Scottish Water, Cambridge Water, Generale des Eaux, and a range of private manufacturing and service businesses. Through monitoring, the typical customer can be expected to save between 5-15% of the cost of a water bill. Qonnectis is currently in development of its next generation monitoring product.” Leakfrog Product This is clearly an important Product in the Qonnectis arsenal - this text is from the Website: “One of Qonnectis’ products is Leakfrog, which was developed in partnership with Thames Water, the UK’s largest water company, and rolled out as part of the Victorian Mains Renewal programme. Leakfrog allows water companies to monitor their domestic customers’ homes for water leaks. Significantly, the Leakfrog product only takes seconds to install. A single meter reader can usually fit over 120 Leakfrog units in a day and then return the following day to read the Leakfrog display which will show the presence and quantity of any leaks. Because a Leakfrog unit can typically be used on thousands of different meters during its 3-year life span, it provides utilities with a very economical leak detection strategy. It therefore also helps reduce water loss as well as help eliminate subsequent damage to buildings and property.” Here is a PDF Datasheet on Leakfrog: http://www.waterintelligence.co.uk/wp-content/uploads/2010/10/Leakfrog_Datasheet_MRV_LR.pdf More on American Leak Detection I made a comment somewhere in this Blog that WATR’s website was a bit poor, but thankfully the Customer-facing ALD Website is a lot more like it - you can see it here: https://www.americanleakdetection.com/ I had to put the following text from the Homepage of the Website in here because it really cracked me up !!: “They came in, investigated with smoke, and fixed the problem. For the first time in two months, my house doesn’t smell like a restaurant toilet”. Sandi T. clearly needs to eat somewhere different….. I found the ALD website very impressive and responsive - it is well worth a good poke around to really understand what WATR can offer. WATR’s Stated Strategy Again this comes from their Website:

Something I notice by its absence is that Leakfrog does not get a specific mention as part of Strategy - I can only assume they see it as just part of a wider Product Set. However, the Strategy does include clear statements on expansion into more Countries and that suggests the possibility of considerable growth in the future. Corporate Structure I copied this bit directly from their Website but it is obviously important: “Water Intelligence plc (formerly Qonnectis plc), which was incorporated in England and Wales (company number 03923150), owns 100 per cent of the issued capital of American Leak Detection Holding Corp. which owns the entire issued capital of American Leak Detection, Inc., the Company’s principal trading subsidiary which operates primarily in the United States.” This sounds complicated and messy but I don’t think it is anything to be concerned about. You will also notice references to ‘Plain Sight Inc.’ especially in the Section below on the Directors of WATR. I found the following from a Google Search: https://www.bloomberg.com/research/stocks/private/snapshot.asp?privcapid=26145627 You will see further down that Plain Sight is a Major Shareholder in WATR which I find slightly strange as Plain Sight is a Subsidiary of WATR and it all seems a bit incestuous. For many this would be a ‘Red Flag’ and keep them away from Investing but I am taking the view that it is something to be aware of and to monitor and if there is any funny business then it might be time to dump the Stock. Listing Details Company Secretary Liam O’Donoghue – Director ONE Advisory Group 201 Temple Chambers 3-7 Temple Avenue London EC4Y 0DT Tel: +44 (0) 20 7583 8304. Registered Office 201 Temple Chambers 3-7 Temple Avenue London EC4Y 0DT. Company Number Registered in England and Wales number 03923150. US Address 888 E. Research Dr., Suite 100 Palm Springs, California 92263 USA t +001 (760) 969-6830. Nomad (Nominated Adviser) finnCap 60 New Broad St London EC2M 1JJ. Nominated Broker WH Ireland Group plc 24 Martin Lane London EC4R 0DR. Auditors Crowe Clark Whitehill LLP St Bride’s House 10 Salisbury Square London EC4Y 8EH, UK. Bankers HSBC Bank Plc 2 London Road Twickenham Middlesex TW1 3RY. Liberty Bank CT USA. Registrar Neville Registrars Limited Neville House 18 Laurel Lane Halesowen West Midlands B63 3DA Tel: 0121 585 1131 Annual Reports You can find the Annual Reports here - going back to 2005 which is nice: http://www.waterintelligence.co.uk/rule-26-investor-relations/documentation/annual-reports-and-accounts/ Risks

In the 2016 Annual Report, the following List of Risks is produced by the Company: “Principal Risks and Uncertainties The Group’s objectives, policies and processes for measuring and managing risk are described in note 23. The principal risks and uncertainties to which the Group is exposed include: Market Risk The Group’s activities expose it to the financial risk of changes in foreign currency exchange rates as it undertakes certain transactions denominated in foreign currencies. There has been no change to the Group’s exposure to market risks. The Group and the Company had no material foreign exchange transactional exposure at 31 December 2016. Interest Rate Risk The Group’s interest rate risk arises from its short and term loan borrowings. Whilst borrowing issued at variable rates would expose the Group to cash flow risks, as at year-end, the Company does not have any variable rate borrowings. Credit Risk The Group’s credit risk is primarily attributable to its cash and cash equivalents and trade receivables. The credit risk on other classes of financial assets is considered insignificant. Liquidity Risk The Group manages its liquidity risk primarily through the monitoring of forecasts and actual cash flows. Other Risks There is a risk that existing and new customer relationships and R&D will not lead to the sales growth. The Group is reliant on a small number of skilled managers. Further, the Group is reliant on effective relationships with its franchisees, especially in the US.” Competition WATR’s main business is in the US and I suspect the Competitive Landscape will be pretty similar in most Countries in which they operate. As always, it is not easy to figure out direct Competitors without more local knowledge and perhaps speaking with WATR Directors might help, but here are a few to consider:

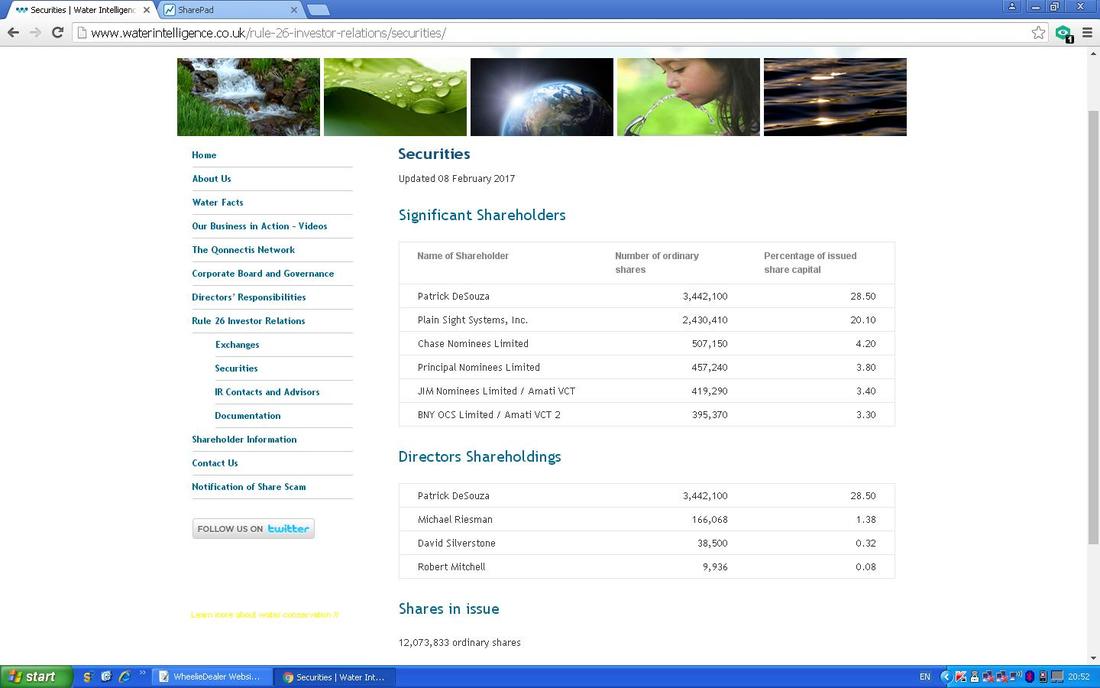

Anyway, ALD claim to be the Number 1 in the US at Leak Detection and Repair and the growth they are achieving sort of lines up with this. Directors The following text is copied from the Website - one thing that hits me is that some members of the Board are quite advanced in years !! “Patrick J. DeSouza, Executive Chairman Dr. DeSouza is President and Chief Executive Officer of Plain Sight and is a graduate of Columbia College, the Yale Law School and Stanford Graduate School. He has 18 years of operating and advisory leadership experience with both public and private companies in the defence, software/Internet and asset management industries. Over the course of his career, Dr. DeSouza has had significant experience in corporate finance and cross-border mergers and acquisition transactions. He has practised corporate and securities law as a member of the New York and California bars. Dr. DeSouza has also worked at the White House as Director for Inter-American Affairs on the National Security Council. He is the author of Economic Strategy and National Security (2000) and has been a visiting lecturer at Yale Law School. David Silverstone, Executive Director David Silverstone, 65, has been involved in water issues since the early 1970’s. He served as Connecticut’s first consumer advocate on utility issues from 1974 to 1977. He then practiced law focusing on utility issues representing water, electric and gas utilities, consumer groups, large consumers and small power producers until 1999. From 1999 to 2000 he was Group Vice-President and Chief Administrative Officer of The Southern Connecticut Gas Company, a local gas distribution company. From 2001 until his retirement in 2008 he was Chief Executive Officer of the South Central Connecticut Regional Water Authority based in New Haven, Connecticut. The Authority has over 400,000 consumers, 1600 miles of pipe, and an annual operating budget of over $75 million . Since his retirement he has been Chairman and Chief Executive Officer of Science Park Development Corporation, a non-profit company charged with the redevelopment of the former Winchester Gun factory in New Haven, a 80 acre site with over 2million sq ft. of space, into a high tech/bioscience mixed use development. Mr. Silverstone graduated from Lehigh University with a B.A, and from Columbia University School of Law with a J.D. He resides in Hartford, Connecticut. Michael Reisman, Non-executive Director Prof. Reisman is a director of Plain Sight and currently serves as Myres S. McDougal Professor of International Law at the Yale Law School, where he has been on the faculty since 1965 and has previously been a visiting professor in Tokyo, Berlin, Basel, Paris, Geneva and Hong Kong. He is a Fellow of the World Academy of Art and Science and a former member of its Executive Council, the President of the Arbitration Tribunal of the Bank for International Settlements, a member of the Advisory Committee on International Law of the Department of State, Vice-Chairman of the Policy Sciences Center, Inc., and a member of the Board of The Foreign Policy Association. He has published widely in the area of international law and served as arbitrator and counsel in many international cases. He was also President of the Inter-American Commission on Human Rights of the Organization of American States, Vice-President and Honorary Vice-President of the American Society of International Law and Editor-in-Chief of the American Journal of International Law. He has served as arbitrator in the Eritrea/Ethiopia Boundary Dispute and in the Abyei (Sudan) Boundary Dispute. John Weigold, Non-executive Director John is currently a senior client partner for Korn Ferry International in the firm’s Industrial practice with a focus on aerospace, defense, and security. He has more than 18 years’ experience finding top-performing senior leadership talent. John also serves as a Rear Admiral in the U.S Navy as Reserve Deputy Commander for the U.S. Pacific Fleet. Robert Mitchell, Non-executive Director Robert graduated from Buckingham University in 1987 with a BSc (Hons) Economics. In 1995 he obtained an MBA from Exeter University. He is a chartered member of the Securities Institute. After a seven year grounding in smaller company analysis and investment at Framlington Investment Management Robert joined F&C Asset Management plc (formerly ISIS Asset Management plc) in 1995 to help launch The AiM Trust PLC and then assist in its management. He was then responsible for launching and managing The AiM VCT PLC and AiM VCT2 PLC as well as managing The Discovery Trust PLC. Robert has considerable experience of investing in AiM, the UK’s junior market, having been involved in it since its inception and having invested in over 250 companies of which the majority have received primary capital from clients he has managed. In 2005 Robert left F&C along with two colleagues to form the specialist smaller companies investment boutique Bluehone Investors LLP. Robert is a non-executive director of Resources in Insurance Group PLC and a Director of Bluehone Holdings PLC.” Director’s Shareholdings The ScreenShot below comes from their Website. Patrick DeSouza, the Chairman, clearly has a large interest and is also a Director of Plain Sight Inc.

Recent Shareholder Dealings

This is perhaps disappointing (although some of the Directors already have plenty of Shares) but I cannot see any recent Trades by Directors except for a Sell by a Former Employee on 12th January 2015 of 800,000 Shares. Having said that, WATR did a Placing back on 24th November 2016 and Michael Reisman, a Non-Exec, bought 18,868 Shares. Details of the Placing and the reasons for it are here: http://www.waterintelligence.co.uk/wp-content/uploads/2016/12/RNS-Number-0047Q.pdf Major Shareholders Here’s a rather excellent ScreenShot I have taken from SharePad - as you can see, this is a pretty sweet representation of this useful information (it also repeats the Director stuff but I thought it useful to keep the earlier bit from the Website in as well because Readers might want to check any updates themselves in the future):

Note the Director Deals that SharePad has here from 6th January 2017 - it is rather strange because I cannot see these on the RNS List on the WATR Website. Anyway, nice to see there are mostly Director Purchases here, not Sells.

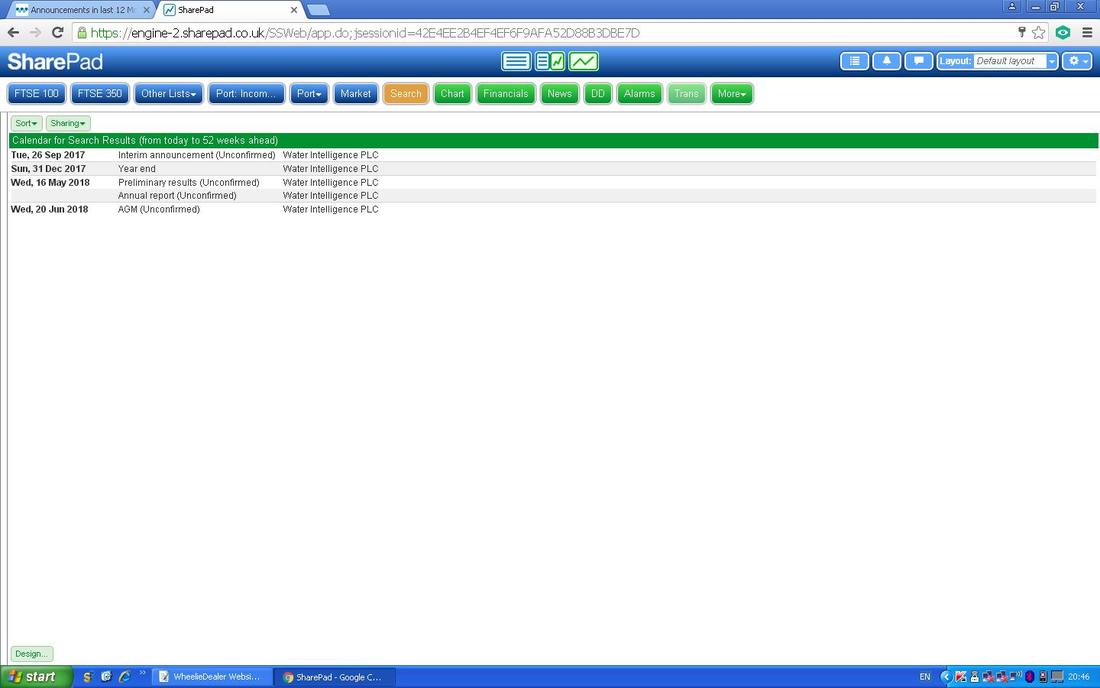

Calendar Again, I have blagged this ScreenShot from SharePad:

It says “Unconfirmed” but my expectation is that the Interim Results at the end of September should be pretty decent and that is why I wanted to buy the Shares well in advance - I often find that Shares run up in advance if the Market is expecting Results to be ok.

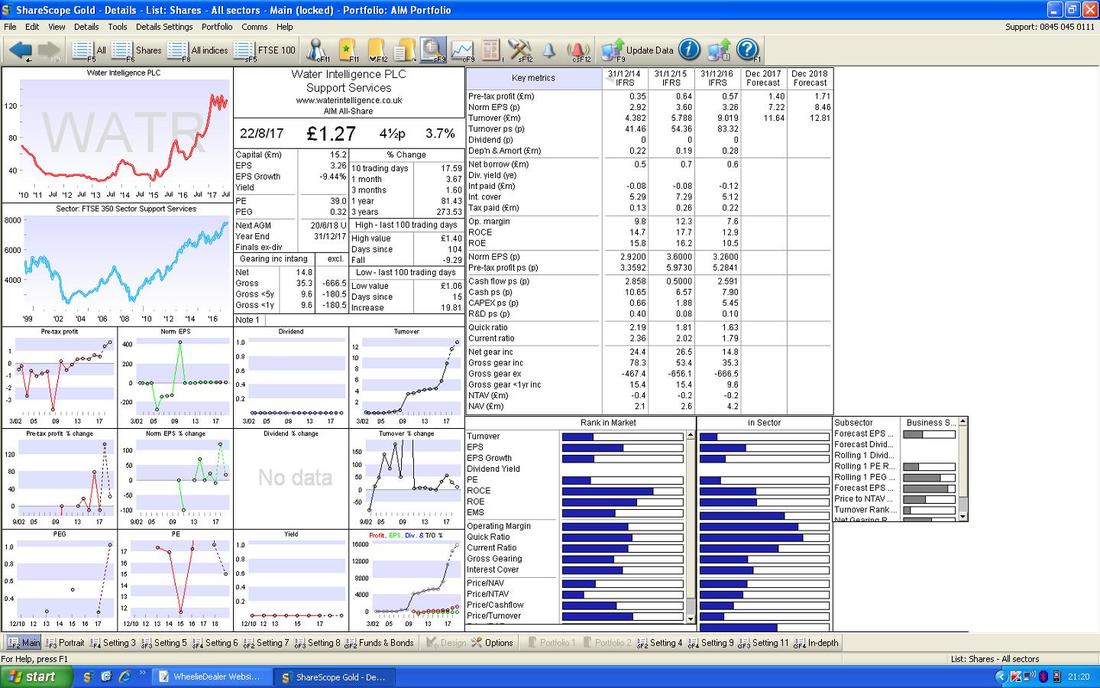

Recent Results WATR released a Trading Update on 9th August 2017 which you can read here - it’s a cracker: http://www.waterintelligence.co.uk/wp-content/uploads/2017/08/RNS-Number-4582N.pdf First off, note that they say First Half Results are due to be released in early September - this contradicts the SharePad Calendar I showed earlier and suggests we will get Interim Results very soon. This sentence near the start stands out to me - I love the word “accelerate” - I don’t see this in many Updates: “This update reaffirms the guidance provided in April that the growth of the business is continuing to accelerate.” This bit sounds great also with a strong growth rate: “Through June, sales reached approximately $8.5 million representing 50% growth over the same period during 2016. This growth path compares favourably with full year 2016 sales growth of 38% (2015: 23%).” This bit is important because WATR have been buying back several of their Franchise Areas: “Sales from ALD's corporate stores are running at 70% growth reaching $3.1 million, demonstrating our ability to accelerate growth in operating units following reacquisition and additional Investment.” Obviously it’s one thing to have strong Sales growth but as they say, “Revenue is Vanity, Profit is Sanity”, so it’s nice to see Profits are in line whilst WATR is investing in growth drivers: “Profits before tax remain in line with expectations, reflecting the Company's choice to fuel further growth through reinvestment in both additional staff and marketing efforts in order to capitalise on the market opportunity in its geographies: United States, United Kingdom, Canada and Australia.” This is nice to see - small growth businesses are always more attractive when they are able to boast a decent Cash Pile and clearly Trading is topping that up through the year: “The Group continues to have sufficient cash reserves to execute its growth plan. Cash at the end of June was a little over $1.0 million, which is consistent with year-end 2016 levels.” And here’s a clear statement of where they think Revenues are headed: “As noted in the 2016 Statement, we continue to believe that the milestone of $20 million in annual sales for Water Intelligence is within sight, up from $7.2 million at year-end 2014.” $20 million at a £/$ Rate of 1.28 is about £15.6m. From the ShareScope ‘Details’ Screen that I show under the ‘Valuation’ section later in this Blog, the Forecast Revenue for 2018 is £12.81m - on this basis, WATR is expecting continuing growth in Revenue after 2018 and I guess it would take about another 2 years to get near that $20m figure, although with Acquisitions etc. maybe they could hit this in 2019 - I don’t think it is particularly an issue either way but obviously it would be better if they hit the £20m number early. There was also an RNS issued on 22nd May 2017 about an Agreement with American Pool Enterprises which looks quite a positive development - you can read it here: http://www.waterintelligence.co.uk/wp-content/uploads/2017/05/RNS-Number-7028F.pdf On 6th February 2017 they signed a nationwide agreement with one of the Top 5 Insurance Companies which you can read here: http://www.waterintelligence.co.uk/wp-content/uploads/2017/05/RNS-Number-7028F.pdf Valuation The ScreenShot below has the ShareScope ‘Details’ Screen for WATR from the 22nd August 2017. If you look in the Top Right Hand Corner you should be able to see ‘Norm EPS(p)’ for ‘Dec 2017 Forecast’ of 7.22p (if you click on the image it should grow huge in your Browser), which is the Current Year and on my Buy Price of 130p, that gives a Forward P/E of 18 (130 divided by 7.22). For ‘Dec 2018 Forecast’ the figure is 8.46p which on my Buy Price of 130p gives a Forward P/E of 15.4, but it is worth bearing in mind that this is Next Year so it is not like we are talking years away and that Forecast looks fairly realistic (especially when considered in the light of their aim to hit $20m of Revenue soon). Just a very rough calculation, the Profit is growing at around 15% per year, so with a Forward P/E of 15 we get a PEG (Price Earnings divided by Growth) Ratio of about 1.0 - anything 1.0 or below is seen as good value. Clearly if WATR can grow faster than this (with Acquisitions this is very possible) then the PEG could slip below 1.0. There is no Dividend as the Company is ploughing any Spare Cash into Expansion - this seems a reasonable thing to do when the Company is so small and Growth is the objective. By the way, the Forecasts are from Finncapp who are the Nomad.

Targets

This bit is utter guesswork really. It is not hard with a few Acquisitions and some Organic Growth to see WATR banging in Earnings Per Share of perhaps 12p in a few years - put this on a P/E Multiple of 15 (this is in line with the current Forward P/E) and you get a Target of 180p (12p x 15) - 38% Upside on my Buy Price. That is pretty realistic, if we get a bit more silly, then maybe 15p of EPS is possible and a P/E Multiple of 18 times - this gives a Target of 270p - so clearly there is plenty to shoot at. Patience will be needed though and I will be monitoring the situation over time and if WATR make the right sort of progress then perhaps I will be adding to my Position. In some ways these Targets are on the conservative side - it is possible that they can beat these Forecasts which look not all that stretching and of course that would give upside. In addition, many Small Growth Companies are on absurd Valuations at the moment (P/E Ratios in the high 20s) and further P/E Expansion could add upside if WATR get a reputation for delivering the numbers. Chart Situation As always, the Charts below are taken from the marvellous ShareScope Software that I use. First off we have the longest Chart I can find in ShareScope going back to late 2010 and the thing to notice here is that since about mid 2015 the Share Price has been moving up and my Black Line (marked with my Black Arrow) is showing the Uptrend Support Line.

On the next Chart I have zoomed in to just the last few Years and again we have the Black Line which is the Uptrend Support and now I have drawn in a Red Resistance Line which needs to be broken-out of. In an ideal world perhaps I should have waited for the Breakout but knowing how Choppy, Illiquid and Volatile this Stock is, I wanted to get in quite pronto once I had some Cash freed up from my Cape CIU Sell. Note I have not done a Spreadbet and although igindex does list one on its Platform, I doubt they actually enable a Long Spreadbet on WATR - it is simply too choppy to be a suitable Spreadbet play really.

On the Chart below you should be able to see a 13/21 Day Exponential Moving Average ‘Golden Cross’ where the Red Line has crossed the Green Line from underneath - where my Blue Arrow is pointing. If you look to the left you can see where a similar Cross happened which my Black Arrow is pointing to. Regular Website Readers will probably recognise these 13/21 Day EMA Crosses from my Weekend Chart updates.

This Golden Cross and the expectation of Interims at the start of September were the main reasons I made my move on WATR now.

Conclusion

If I have achieved my aim, then this Blog should have given Readers a good insight into what WATR is all about. It is clearly a Very High Risk Stock and not one I would want to buy loads of at this stage, but maybe in the future I can add to my Position as the Story develops. In summary, the reasons I like WATR are as follows:

The Big Risk here is around the Share itself and the lack of liquidity and wide Spread - I have managed this by only putting around 1% of my Portfolio into the Stock at this stage - I might add more over time. Regards, WD.

2 Comments

John Kyle

25/8/2017 10:52:42 am

Great Research WD and Good Luck with WATR!!

WheelieDealer

26/8/2017 10:48:07 pm

Thanks John, hopefully the research and purchase will pay off nicely - WATR certainly looks promising and I reckon my thoughts on growth etc. could be on the low side. Leave a Reply. |

'Educational' WheelieBlogsWelcome to my Educational Blog Page - I have another 'Stocks & Markets' Blog Page which you can access via a Button on the top of the Homepage. Archives

January 2021

Categories

All

Please see the Full Range of Book Ideas in Wheelie's Bookshop.

|