|

educational blogs |

|

THIS IS NOT A TIP. I AM NOT A TIPSTER. PLEASE DO YOUR OWN RESEARCH. PLEASE READ THE DISCLAIMER ON THE HOME PAGE OF MY WEBSITES.

A couple of weeks back on the 23rd March 2015, I topped up on my Tristel TSTL holding at 73p after some superb Results. I have been in this Company for quite a while - maybe even a year, but I like the story here and it really strikes me that they are increasingly gaining acceptance with Customers with regard to their Infection Control offerings. It is quite a small Company, with a Market Cap around £30m and is listed on AIM. This makes it inherently Risky and I have put about 2.5% of my Total Portfolio Value in it. I expect to hold this for the Long Term - and maybe several years if all goes to plan.

Company Overview

TSTL Develops and Manufactures Chlorine Dioxide based Infection Control Products targeted at the following Market Subsectors:

The Products are Repeat Use Consumables, which means once they gain acceptance by Customers there are regular repeat orders. The Products tend to be ‘Sticky’ - once a Customer is happy with the Products and used to working with them, they tend not to change. The Company has 100 Patents and others pending, and roughly 75% of Products are Patent Protected until 2028-2029. For more detail on TSTL’s Products, please click this link: http://www.tristel.com/products/ I found some of the Information on the Website confusing. At one point it says that the Animal stuff is sold under the Anistel Brand, but then I found elsewhere that there are Brands like Dermastel, Enzystel, Medistel, Airstel and Odostel. It struck me that the Company’s Website is a bit rubbish really - seems like they could do with focusing some effort on improving this. The conventional view of TSTL is that they do Infection Control Wipes for Endoscopes - but having poked around the Website, I think this is simplistic and in fact they do a huge amount more than this. The Wipes are used for Instruments but they also do a range of stuff for Surfaces. They also seem to do some Legacy Products that are not Chlorine Dioxide based - I understand from the most recent Trading Update that they will be winding these down and focusing efforts on the Chlorine Dioxide stuff - this seems like a very sound Strategy. However, the Wipes are clearly a key part of their success, with their method being the most widely used in the NHS for ENT, Cardio and Ultrasound. TSTL also provide Liquids, Foams, Sprays and Gels for Surface Cleansing and Decontamination and the Chlorine Dioxide method works against MRSA (meticillin-resistant staphylococcus aureusis), C-Diff (Clostridium Difficile) and Norovirus. Human Products account for about 60% of Revenues. The Company was formed in 1993 and listed on AIM in 2005. A Manufacturing Plant in Cambridge, UK, was completed in 2007 and at the end of September 2014 they expanded the Factory, Offices and Warehouse capacity. The Anistel Brand was created in 2012. TSTL’s products are sold in over 25 countries. In most countries the products are sold through a national distribution partner, however, TSTL has its own operations in the following countries:

The Company’s Website can be reached via this link: http://www.tristel.com/ There are some interesting Case Studies here which give an indication of how attractive TSTL’s Chlorine Based Products are: http://www.tristel.com/resources/case-studies/ Interim Results TSTL released Interim Results on the 25th February 2015. You can read them here: http://www.tristel.com/investors/financial-performance/interim-accounts/ I found this a very positive Statement and it tipped me over the edge to buy more - I really think the Company is on a Roll and has the potential to be a great Growth Stock over many years. The bits that stood out for me here were:

Directors

Director Shareholdings The interests of the directors in the shares of the Company at 31 December 2014 were:

The total number of shares not held in public hands at 31 December 2014 was 12,182,735, constituting 29.95% of the company’s share capital. I think this means that 30% of the Shares are held by the Directors !! It’s fair to say they have ‘Skin in the Game’. Substantial Shareholders From the Company’s Website, the following were interested in 3% or more of the Company’s equity at 31 December 2014:

Risks

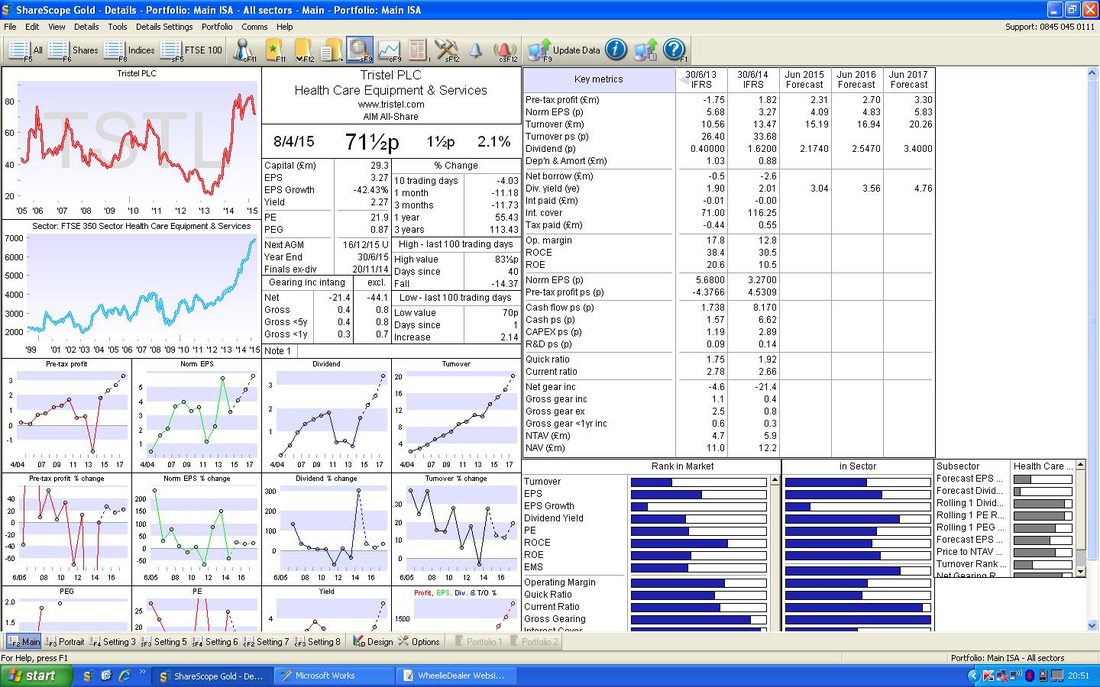

Valuation Right, now we get to the fun bit for me - a lot of the previous stuff is quite tedious to write, but now we are getting to the Good Stuff (as Paloma Faith would say). For Next Year (2016), ShareScope is showing Consensus EPS (Earnings Per Share) Forecasts of 4.83p. At the Price I recently paid of 73p, this means a P/E Ratio of 15.1. For Next Year (2016), the Forecast Consensus Dividend Per Share is 2.54p. At my 73p Buy Price, this gives a Dividend Yield of 3.5%. It is worth appreciating that these figures are before you strip Cash out from the Share Price - this would make the figures slightly more attractive. From a quick look at the Forecast Numbers, it seems fair to say that Growth of about 15% per year is reasonable. This would put the Stock on a PEG (Price Earnings / Growth) Ratio of about 1.0 (usually anything below 1.0 is seen as Cheap). So, from these Figures, TSTL does not look especially screaming Value. However, it is clearly not Expensive. The ScreenShot below shows the ShareScope Details screen - the Forecast Consensus numbers are in the Top Right Hand Corner.

Target

I see TSTL as very much a Long Term Growth Story and I expect to hold the Stock for many Years. In the Short Term, my expectation is that they will continue to deliver good results and the Market will award them with a Higher P/E Rating. In addition, I expect to see them beating Expectations as the Operational Gearing kicks in. To give an indication of what this means, let’s assume the P/E Rating for Next Year (2016) rises to 18 - this would give a Target Price of 87p (4.83p x 18). If we look at the Consensus Forecast EPS for 2017 of 5.83p and put it on a P/E of 15, we get a Target Price of 87p again. However, if we up the P/E to 18 as before, then the Target Price would be 105p. It is not hard to see that in a few years, the Stock could be producing EPS of 8p and if we give that a Multiple of 18, we get a Target Price of 144p. OK, that is rather fanciful but there are two things to bear in mind here - firstly, I have not allowed for the Cash Pile and secondly, they have a habit of Beating Expectations. It might even be possible to see a P/E of 20 - this would mean a Target Price of 160p. In addition, it is not hard to see a Dividend of 6p a Share (the Consensus Forecast for 2017 is 4.66p), which would give a Dividend Yield of 8.2% on the Price I paid of 73p. Another Opinion Simon Thompson from Investors Chronicle recently commented on TSTL and has put a Target of 100p on it. He also suggests that Current Year Forecasts could be beaten and that the Company has a history of beating Forecasts. Many people have a dim view of Simon Thompson, but I find that apart from his Resources Junk and the Brain Fade he suffered over Chinese Stocks, he is actually very good when he sticks to simple UK Companies. Technicals As ever, I will whizz through the usual Charts and Indicators. On the Chart below, you should see a couple of years with a nice Uptrend and now a ‘Pennant’ kind of pattern. The hope here is that the Share Price can pop out of the Red Top Line (marked with the Green Arrow) and this would be a very Bullish event. Dropping through the lower Black Line (marked with the Blue Arrow) would not be welcome. However, as a Long Term Investor, I will be sticking with it unless something goes horribly wrong in the Business itself.

On the Chart below you should see a Blue Circle which highlights a Double-Candlestick formation which is a ‘Bullish Harami’ - think of a Pregnant Lady viewed from the side. This is the Chart from Close of Play today (8th April 2015) and after the Down Wave of the last 4 weeks or so, this is a Bullish Signal that the Price could rise now. I bought more about 2 weeks ago.

If you look at the Bottom Window of the Chart below, the Green Arrow is pointing out that the RSI (Relative Strength Index) is Low and this usually means the Price will rally.

On the Chart below, please look at the top Window, where you can see the Bollinger Bands. My Blue Arrow here is pointing out that the Price is touching the Bottom Bollie Band and this could mean the Price will move up soon - although it is not a perfect Indicator as Prices can ‘hug’ Bollie Bands for a while. The best Buy signal would be if the Price starts to move clearly up off, and away from, the Bottom Bollie Band.

On the Chart Below, note my Green Arrow which points out how the Price has touched the 305 Day Moving Average - this is a 10 Month Line. If is an area of Strong Support so could be a good point to Rally from.

The Chart Below shows the Weekly Candles, rather than the Daily Candles. In this case, I am pointing out that last Week the Price Action produced a ‘Long Tails Doji’ which is a good Reversal Signal after the Downmove of Recent Weeks - shown by the preceding Red Candles. Please ignore the Red Candle right at the far Right Hand Side of the Screen - this is for the Current Week and is not a Full Candle yet - wait until Friday !!

Conclusion

It is pretty obvious that Infection Control in Healthcare environments (be it Human or Animal) is a major issue. TSTL seem to be creating a nice little niche and their Chlorine Dioxide based Products are clearly gaining wide Acceptance. With the well-publicised problems around overuse of Antibiotics, it seems a near certainty that Infection Control will be a big issue for many years to come. TSTL seems to play nicely into this larger Theme and there are few other Stocks that offer such Potential at this kind of Valuation. The recent expansion of capacity at the Cambridge Plant is a clear sign that the Directors believe there is a growing Demand for their Products. There is also a bit of potentially huge Upside from a possible move into the US. Management seem to give the impression that they would like to make the move at some point, but obviously it has massive Cost Implications due to the need to get the Products approved by the FDA (Food and Drugs Administration). In fact, they are already getting Enquiries from US Hospitals who would like to use their Products. I think it is quite likely that they will get snapped up by a Larger Group - Infection Control is an area of extreme Political Importance and Big Players will be keen to get hold of a Leading Technology as it gains wider acceptance. Cambridge is a hotbed of Pharma and Biotech Groups and TSTL will be very well known within that Local Industry. TSTL is clearly not screaming Value here but I think it is very much a Growth Story and certainly represents ‘Growth at a Reasonable Price’ (GARP). I think Patience will be required here but a Target of 100p should be fairly easy. In time, I expect 120p and more. In addition, I will pick up nice Dividends on the way. 120p would be 64% Upside on my recent 73p Buy Price. Dobry wieczór, wd

0 Comments

Leave a Reply. |

'Educational' WheelieBlogsWelcome to my Educational Blog Page - I have another 'Stocks & Markets' Blog Page which you can access via a Button on the top of the Homepage. Archives

January 2021

Categories

All

Please see the Full Range of Book Ideas in Wheelie's Bookshop.

|